Two Japanese industrial buyers contacted BioEconomy Solutions this month — not through a broker, not through a trade show — directly. Hunting for American paulownia. Willing to talk volume. Willing to talk long-term.

That doesn’t happen by accident.

When one of the world’s most disciplined, quality-obsessed timber markets starts calling a paulownia farm in the American South, something structural has broken in the global supply chain. And the window to position yourself on the right side of that break is closing faster than most people realize.

Here is exactly what is happening — and why it matters to every landowner, carbon developer, and ESG investor paying attention to the bioeconomy right now.

PART A: STAKES — Why Should You Care?

Most people in the American timber and carbon markets have never thought about Japan’s paulownia problem.

That is precisely why this is an opportunity.

Japan is not a casual buyer. When Japanese industrial procurement teams start making direct international calls, it means their domestic supply chain has already failed them. It means their regional brokers have already let them down. It means they are in a structural squeeze — not a seasonal dip — and they need a reliable partner, not a spot-market gamble.

Let’s put the scale of this in context.

Japan has historically imported up to 70% of its paulownia supply. The tree — known in Japan as kiri — is not a commodity wood. It is a cultural and industrial cornerstone. It is used in:

Tansu cabinetry — the centuries-old Japanese chest tradition, where paulownia’s natural moisture-regulating properties protect silk kimonos and heirlooms

Koto musical instruments — Japan’s national stringed instrument, where the resonance and tonal properties of paulownia are irreplaceable

High-tech lightweight laminates — aerospace-adjacent industrial applications where paulownia’s unmatched weight-to-strength ratio and near-zero shrinkage make it the only viable natural material

Precision industrial crating and packaging — where its dimensional stability protects sensitive electronics and precision components during export

This is not a market that substitutes easily. You cannot swap paulownia for pine and call it done. The physical specifications — bone-dry consistency, tight grain, uniform density, low shrinkage — are non-negotiable for Japanese buyers.

And right now, those specifications are becoming impossible to source at scale.

The cost of inaction for Japanese buyers is not inconvenience. It is production shutdown.

PART B: STORY — What Is Actually Breaking the Supply Chain?

Three forces have converged simultaneously to create this crisis. Understanding all three is critical — because together, they are not a temporary disruption. They are a permanent structural realignment of where paulownia will be grown and traded for the next two decades.

Force #1: The Global Supply Chain Shock

A significant portion of Japan’s imported paulownia has historically originated from or processed through manufacturing hubs in East Asia. That pipeline is fracturing.

Escalated conflicts in the Middle East have caused a massive squeeze on crude oil and petrochemical derivatives — specifically naphtha, the feedstock for styrofoam, plastic foams, and synthetic protective packaging materials. Japanese domestic industries are facing critical shortages of the petroleum-derived packaging and insulation materials they have relied on for decades.

When synthetic packaging spikes in price or faces order suspensions, Japanese industries do not wait. They pivot. They lean back into what they know works — natural wood alternatives for high-end crating, precision packaging, and stable structural components.

Paulownia is at the top of that list.

The demand surge is not coming from one sector. It is coming from electronics manufacturers, precision instrument makers, traditional craft industries, and construction component suppliers — all simultaneously competing for a shrinking pool of available kiri stock.

The ripple effect is real. The demand is not speculative. It is already here.

Force #2: Decades of Domestic Depletion

Japan’s domestic paulownia supply has been in a multi-decade decline. This is not a new problem — but it has now reached a critical threshold.

An aging forestry workforce, land-use shifts toward urban development and rice cultivation, and the collapse of traditional rural forestry management have gutted Japan’s ability to self-supply. What was once a thriving domestic kiri industry has been reduced to a fraction of its former capacity.

For years, Japan compensated by importing from Southeast Asia and regional East Asian suppliers. That pipeline is now tightening too — rising production costs, inconsistent quality control, and geopolitical friction are making those traditional sources unreliable.

Japanese buyers are not looking for a short-term fix. They are looking for a long-term supply chain partner — one with the land, the infrastructure, the climate, and the operational discipline to deliver consistent, scalable, specification-grade paulownia year after year.

The United States — specifically the American South — is one of the very few places on Earth that can credibly offer all of that.

BioEconomy Solutions’ hybrid paulownia program in South Carolina produces non-invasive, non-GMO, seed-sterile clones specifically engineered for tight grain, uniform density, and the kind of dimensional stability that Japanese buyers require. These are not wild-harvested trees. These are purpose-grown, specification-matched feedstocks — the American equivalent of Japan’s Reference Wood standard.

That is exactly what a supply-starved Japanese market needs to de-risk their supply chain.

Force #3: Currency Volatility Forcing Safe-Haven Purchasing

The third force is financial — and it is accelerating everything.

The Japanese Yen has faced immense pressure in recent months, briefly dipping to 160 JPY to the USD before massive multi-billion-dollar interventions by Japan’s Ministry of Finance stabilized it back to the 155 range. That kind of volatility — a 10%+ swing in the world’s third-largest economy’s currency — does not just affect tourists and exporters. It fundamentally changes how industrial procurement teams think about risk.

When your currency is this volatile, spot-market purchasing from fragmented regional brokers becomes a liability. Every purchase is a currency bet. Every shipment is a hedge that might not pay off.

The response from sophisticated Japanese industrial buyers is predictable and rational: lock down direct, secure supply chain partnerships with established North American feedstock operators. Hedge against future currency and supply shocks by securing volume commitments, predictable pricing structures, and direct relationships with producers who can guarantee consistency.

This is not a trend. This is a structural shift in how Japanese timber procurement works.

And BioEconomy Solutions is already receiving the calls.

PART C: SHIFT — The Lesson That Changes Everything

Here is what this moment teaches us — and it goes far beyond paulownia.

The global bioeconomy is not a future concept. It is a present reality being shaped right now by supply chain fractures, geopolitical disruptions, currency volatility, and the irreversible depletion of traditional natural resource pipelines.

The companies and landowners who position themselves correctly in the next 24 months will not just participate in this market. They will define it.

For too long, the narrative around paulownia in North America has been focused almost entirely on carbon credits and domestic timber markets. Both are real and valuable. But the Japanese inquiry changes the frame entirely.

This is not just a carbon story. This is a global supply chain story.

American-grown paulownia — produced at scale, to specification, with the consistency and traceability that international industrial buyers demand — is a strategic asset in a world where natural material supply chains are fracturing everywhere at once.

The lesson is this: When the world’s most quality-obsessed timber market starts calling your farm directly, you are not just a tree grower. You are a supply chain solution.

The question is whether you are ready to operate at that level.

BioEconomy Solutions is building the infrastructure — the plantation capacity, the drying and grading systems, the blockchain-verified traceability, and the direct buyer relationships — to be exactly that solution. Not just for Japan. For every market where the old supply chains are breaking and new ones need to be built.

The tree grows fast. The window to position is not.

BRICK 3 — BOOST THE SHARE (Shareability + CTA)

The bottom line:

Japan’s kiri crisis is not a niche story for timber traders.

It is a signal — one of the clearest signals we have seen — that the global demand for specification-grade, sustainably produced, traceable natural materials is accelerating faster than supply can respond.

Three forces are driving this simultaneously:

A petrochemical supply shock pushing industrial buyers back to natural wood alternatives

Multi-decade domestic depletion leaving Japan structurally dependent on foreign supply

Currency volatility forcing long-term direct partnerships over fragmented spot-market purchasing

American paulownia — grown right, graded right, and delivered with the consistency international buyers require — is positioned to fill a gap that no other supplier in the world is currently equipped to fill at scale.

BioEconomy Solutions is already in those conversations.

If you are a landowner, carbon developer, ESG investor, or industrial buyer who wants to understand what this supply shift means for your operation or portfolio — let’s talk.

The calls from Japan are already coming in.

The question is: will you be part of the supply chain that answers them?

What’s the biggest barrier you see to scaling American paulownia for international industrial markets? Drop it in the comments — I read every one.

Interested in exploring paulownia supply chain partnerships, carbon credit development, or plantation investment?

Paulownia Secret Weapon Against Eucalyptus Legacy of Depletion

The $2 Trillion Tree Battle: Eucalyptus vs. Paulownia—Which One is Actually Restoring Our Planet?

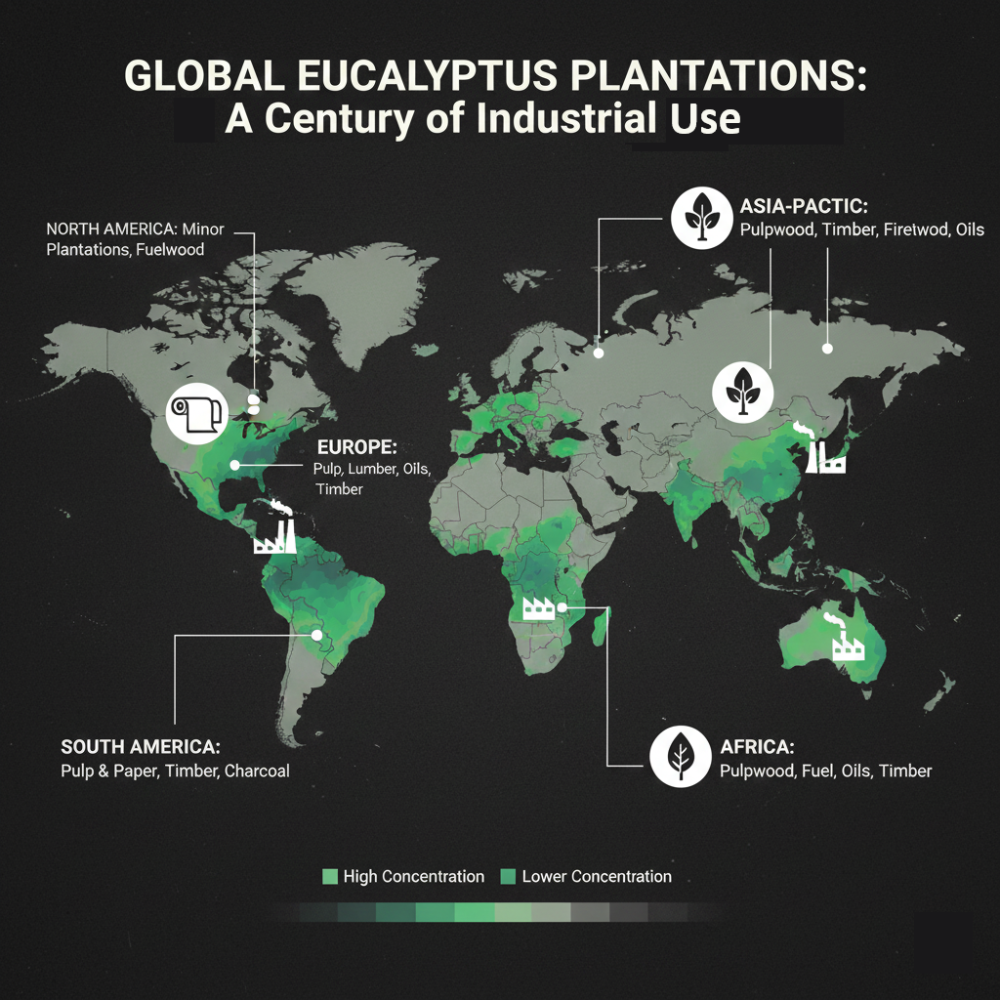

Eucalyptus Tree Around The World

What if I told you that the tree planted across around the world to “solve” deforestation is actually causing it?

Large industries, primarily the pulp and paper and timber industries, have planted extensive eucalyptus plantations around the world. These plantations are concentrated in regions where the fast-growing trees can be used as a renewable resource.

The main geographies and industries involved are:

South America

This region is a global leader in eucalyptus plantations, mostly for the pulp industry.

Brazil: The world’s largest producer of eucalyptus, with millions of hectares of plantations. Major corporations drive the industry, primarily for the production and export of pulp used in paper products. The timber industry also uses the wood for charcoal and solid wood products.

Argentina, Chile, and Uruguay: These countries also have significant eucalyptus plantations, with the pulp industry being the main driver in Uruguay and Argentina, and the timber industry also being significant.

Asia-Pacific

This region has seen rapid expansion in eucalyptus planting, with a significant share of the world’s total.

China: China has developed large areas of eucalyptus plantations for timber production, pulp and paper, and as a source of industrial oils.

India: Plantations are extensive in India, contributing to both the pulp and paper industry and local uses like firewood.

Indonesia: Eucalyptus is a key raw material for the pulp and paper production in this country.

Europe

Eucalyptus is a key industrial resource in parts of Europe, particularly the Iberian Peninsula.

Portugal and Spain: Large areas are dedicated to growing eucalyptus for pulp production, as well as for lumber, veneer, and eucalyptus oil extraction.

Africa

The tree has been widely introduced and used for various industrial purposes.

South Africa and Eswatini: Eucalyptus is grown extensively for pulpwood, poles, fuel, and the extraction of essential oils.

Ethiopia: Historically, it was used to meet a high demand for firewood and construction timber.

North America

While less dominant than other regions, some areas have industrial plantations.

United States (primarily California and Hawaii): Historically introduced for potential timber and railroad ties, commercial planting today is minor compared to global leaders, with some areas studied for pulpwood or industrial fuelwood.

The Global Map

The Background

In Africa referred to as The $792 Million Mistake: Why Africa’s Big Industry Planted the Wrong Tree.

For over 150 years, eucalyptus has been promoted as the miracle tree—fast-growing, drought-resistant, perfect for timber and fuel.

Governments planted it. NGOs funded it. Farmers adopted it.

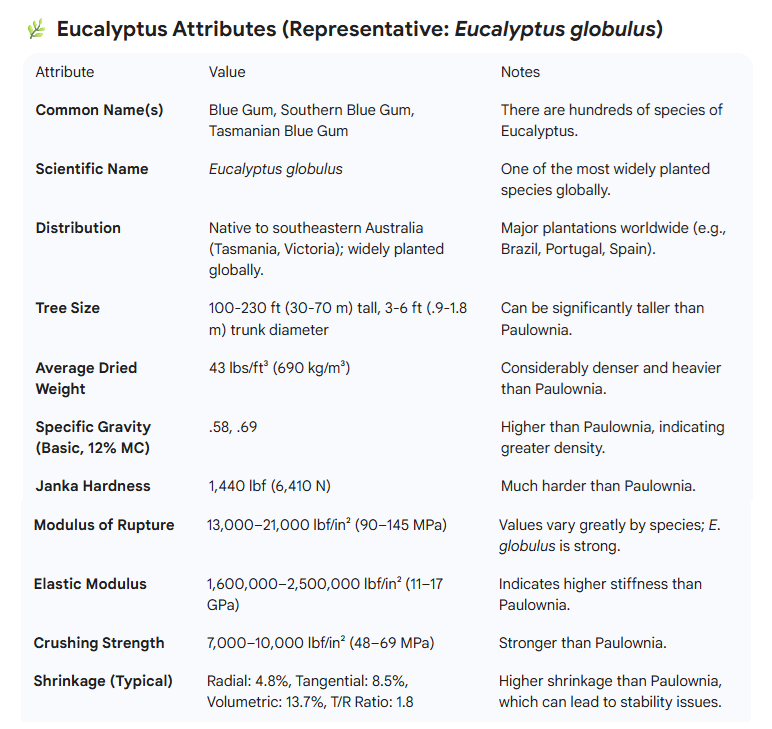

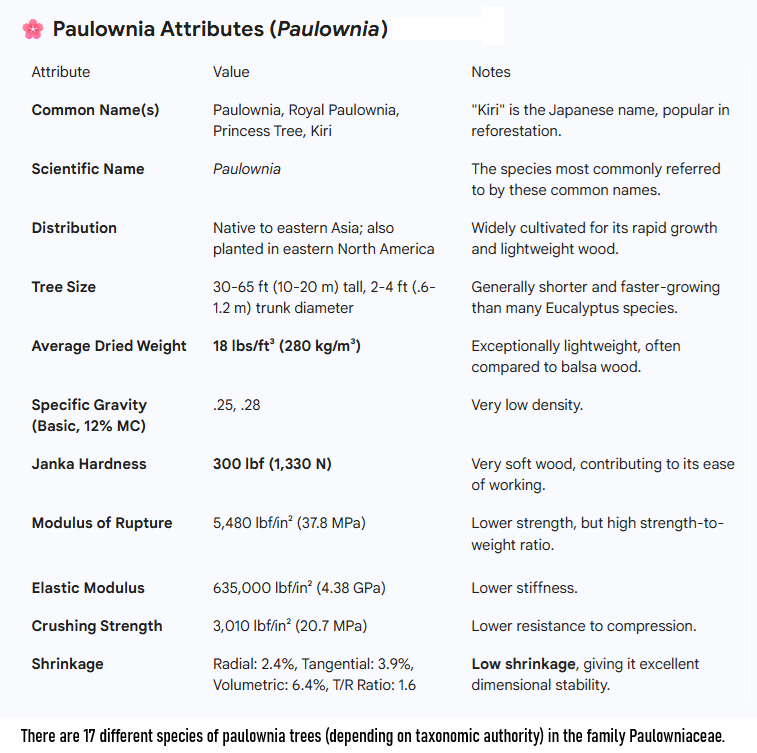

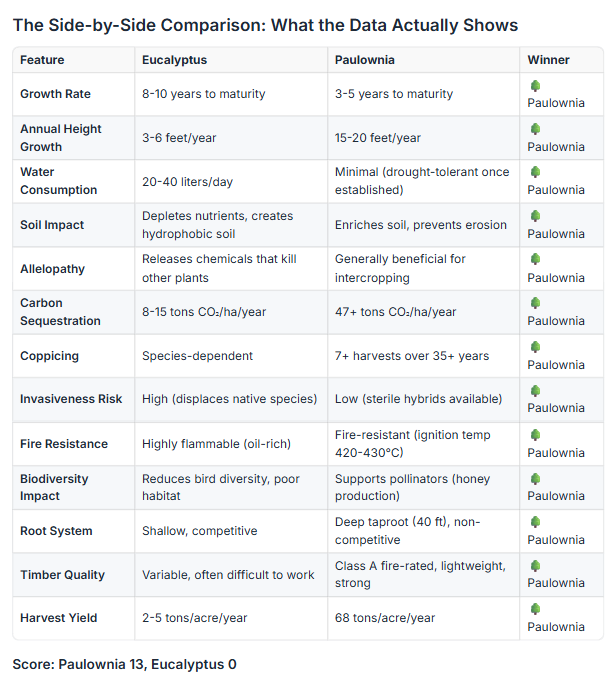

The Wood Value Comparison: Eucalyptus vs. Paulownia

Eucalyptus Wood Value – BY THE NUMBERS

By the numbers Paulownia vs Eucalyptus

What They Did NOT Know?

But here’s what nobody told them:

❎ Eucalyptus trees drink 20-40 liters of water per day.

❎ They release chemicals that kill surrounding crops.

❎ They turn soil hydrophobic (water-repelling).

Meanwhile, there’s another tree—one that grows even faster, uses 90% less water, actually improves soil health, and could save the Big Industry $660 million annually Zimbabwe.

But almost nobody knows about it.

Let me show you the data.

After 40+ years of forestry research, partnerships with CREA Italy and the Chinese Academy of Forestry, and analyzing deforestation patterns across Zimbabwe, Malawi, Tanzania, and beyond, we’ve uncovered a fundamental mistake in how Africa approaches fast-growing trees.

This isn’t about vilifying eucalyptus in its native Australia—it’s about understanding why a tree that works in one ecosystem becomes destructive in another, and why there’s a scientifically superior alternative that’s been hiding in plain sight for 1,000 years.

The Tale of Two Trees: Eucalyptus vs. Paulownia

How Eucalyptus Became Africa’s “Go-To” Tree (And Why That Was a Mistake)

The History:

1850s-1900s: Eucalyptus introduced globally from Australia after Captain Cook’s expeditions

Promoted for: Fast timber, fuel, swamp drainage, malaria control, windbreaks

California Gold Rush: Planted for railroad ties (wood proved too difficult to work)

Portugal (late 1800s): Planted to reforest stripped land—became most common tree

Africa (1900s-present): Widely adopted for commercial timber and fuel

The Promise:

✅ Fast growth (8-10 years to maturity)

✅ Drought-resistant

✅ High timber yield

✅ Medicinal properties (eucalyptus oil)

The Reality:

❌ Water depletion:20-40 liters per day per tree

❌ Allelopathy:Releases chemicals that kill surrounding plants

BioEconomy Solutions (BES) is pioneering the transition from destructive eucalyptus monocultures to regenerative paulownia plantations through The G.U.A.R.D.I.A.N. Framework™. With 40+ years of paulownia research and partnerships across three continents, BES is working with Africa’s tobacco industry to eliminate deforestation while saving $660M+ annually and achieving net-zero operations.

The Princess Tree Paradox: Why the Internet Got Paulownia Completely Wrong

A BioEconomy Solutions Response to the Viral “Invasive Tree” Narrative

The internet just called one of the world’s most valuable trees a villain.

And 99% of people believed it without asking a single question.

A popular YouTube video titled “This Invasive Tree is Named After Russian Royalty!” has been circulating widely, painting the Paulownia tree as an ecological menace — a fast-spreading invader threatening native plant communities across North America. The video is well-produced, the narrator is knowledgeable, and the identification content is genuinely useful.

But here is the problem.

The video talks about one species out of seventeen.

And in doing so, it has contributed to one of the most damaging misconceptions in modern agroforestry, sustainable agriculture, and carbon sequestration science. A misconception that is costing landowners, investors, governments, and communities around the world billions of dollars in missed opportunity.

We are not here to attack the video creator. We are here to set the record straight.

Because when a tree is being planted in over 60 countries, used in United Nations carbon credit plantations, studied by CABI in Wellington, UK, and recognized by the FAO International Commission on Fast-Growing Trees as one of the most promising species for sustainable development — it deserves more than a one-sided narrative built on a single species out of seventeen.

So let us break this down. Brick by brick.

PART A — STAKES: Why This Misconception Costs the World

Before we get into the science, let us establish why this matters beyond a simple YouTube comment section debate.

The global carbon credit market is projected to grow from $8 billion to over $200 billion in the next six years. Nature-based solutions, including fast-growing tree plantations, are at the center of that growth. Corporations with net-zero commitments, governments under Paris Agreement obligations, and institutional investors seeking ESG-compliant assets are all looking for verified, scalable, nature-based carbon removal solutions.

Paulownia — specifically non-invasive hybrid and elongata species — sits at the intersection of every single one of those needs.

It is one of the fastest-growing hardwood trees on the planet. It sequesters carbon at rates that dwarf most other species. It coppices — meaning it regrows from its own stump after harvest — up to seven times without replanting. It improves degraded soil. It supports biodiversity through intercropping. It produces premium timber, biochar, biomass for green energy, honey, animal fodder, medicinal compounds, and more.

And yet, because of the widespread conflation of P. tomentosa with the entire Paulownia genus, landowners are hesitant to plant it. Investors are cautious about funding it. Regulators in some regions have placed blanket restrictions on it. And the general public, armed with a YouTube video and a Google search that surfaces the same tomentosa-focused content over and over again, dismisses it entirely.

The cost of this misconception is not just financial. It is environmental.

Every year that Paulownia plantations are delayed because of misinformation is another year that degraded land goes unrestored. Another year that carbon stays in the atmosphere. Another year that rural communities in Africa, Asia, South America, and the American South miss out on economic transformation.

That is the real cost of getting this wrong.

Paulownia Tomentosa “BLACK SHEEP” Of Paulownia Family

PART B — THE STORY: What the Video Got Right, and Where It Went Wrong

Let us be fair. The video does several things well.

The identification content for Paulownia tomentosa is accurate and detailed. The narrator correctly describes the heart-shaped leaves, the vanilla-scented purple flowers, the distinctive bark patterns, the hollow chambered pith, and the aggressive stump sprouting behavior. For someone trying to identify and manage P. tomentosa on their property in the eastern United States, this video is genuinely useful.

The historical context is also largely accurate. P. tomentosa was introduced to Europe in the 1830s by the Dutch East India Company. It arrived in North America shortly after, initially for silviculture and ornamental purposes. Its seeds were famously used as natural packing material for glassware shipped from Asia, which contributed to its naturalization across the eastern United States.

The video correctly notes that P. tomentosa can invade disturbed areas, produce enormous quantities of seeds, and regrow aggressively from stumps and roots. In the context of managing this specific species in North American native plant communities, these are legitimate concerns.

But here is where the narrative breaks down.

The video never once mentions that there are 17 different species of Paulownia.

Not once.

It never distinguishes between P. tomentosa and P. elongata, P. fortunei, P. kawakamii, or any of the other confirmed species. It never mentions the non-invasive hybrid varieties that have been specifically developed for commercial cultivation. It never references the CABI document prepared for United Nations countries that explicitly accepts P. elongata as a non-invasive species for carbon credit plantations. It never acknowledges that the invasive behavior it describes is largely dependent on the presence of sterile soil — construction sites, burn areas, road cuts — and that Paulownia rarely colonizes open fields because of naturally occurring soil fungi.

Instead, it presents a single species narrative and applies it to the entire genus.

This is the equivalent of saying that because one variety of apple is toxic, all apples should be avoided. Or because one breed of dog is aggressive, all dogs are dangerous. The logic does not hold, and in the case of Paulownia, the consequences of that flawed logic are significant.

THE 17 SPECIES REALITY

Let us be very specific about what the Paulownia genus actually contains.

According to taxonomic authorities, there are between 6 and 17 species of Paulownia in the family Paulowniaceae. The confirmed and tested species include:

Paulownia kawakamii — native to Taiwan, smaller stature, deep purple flowers

Paulownia tomentosa — the Princess Tree, the one species listed as invasive in some areas

Paulownia x taiwaniana — natural hybrid between P. fortunei and P. kawakamii

Paulownia elongata — extremely fast-growing, ideal for intercropping and carbon sequestration

Paulownia fargesii — valued for timber production

Paulownia fortunei — the Dragon Tree, native to southeast Asia, rapid growth, tall stature

Additionally, there are numerous potential variety, hybrid, and synonym species including P. glabrata, P. grandifolia, P. imperialis, P. australis, P. lilacina, P. longifolia, P. meridionalis, P. mikado, P. recurva, P. rehderiana, P. shensiensis, P. silvestrii, P. thyrsoidea, P. duclouxii, and P. viscosa.

Of all of these species, only P. tomentosa is listed as invasive in some areas of the world.

The video discusses only P. tomentosa. But the title, framing, and general narrative create the impression that “Paulownia” as a whole is an invasive problem. This is the core of the misinformation.

WHAT CABI ACTUALLY SAYS

The Collaborative International Agricultural Biodiversity Institute (CABI), based in Wellington, UK, prepared a comprehensive compendium on Paulownia specifically for the purpose of identifying the Paulownia elongata species for use in United Nations countries for carbon credit plantations.

This is not a fringe document. This is a globally recognized scientific institution preparing guidance for UN-level carbon development projects.

The document does state that “Paulownia is categorized as an invasive exotic.” And yes, that line exists. But the full context of that statement is critical, and it is worth quoting in full:

“Paulownia is categorized as an invasive exotic. Although there is little doubt that it is an exotic, the question of its invasiveness is open to conjecture. The many small seeds of Paulownia are windblown. However, the seeds do not germinate and survive unless the seed falls on sterile soil. New germinates of Paulownia have a high rate of mortality from damping-off disease caused by a variety of soil fungi. Generally, Paulownia does not colonize open areas unless sterile soil is present, as in construction activities, recent burned areas and road cuts. Rarely does Paulownia colonize fields, because of the ever-present fungi.”

Read that again carefully.

The seeds do not germinate and survive unless they fall on sterile soil. New seedlings have a high rate of mortality from naturally occurring soil fungi. Paulownia rarely colonizes fields because of those fungi.

This is a dramatically different picture from the one painted in the video, where 20 million seeds per year sounds like an unstoppable ecological invasion. The reality is that the vast majority of those seeds never survive to become established trees. The conditions required for successful naturalization are far more specific and limited than the video implies.

And critically, the CABI document accepts P. elongata as a non-invasive species in all United Nations countries for the purpose of carbon credit plantation development.

THE RESEARCH CONFIRMS IT

The academic research on Paulownia is extensive and largely positive. Dr. Nirmal Joshee of Fort Valley State University, whose comprehensive chapter on Paulownia appears in the Handbook of Bioenergy Crop Plants, notes that:

“Except for P. tomentosa, most Paulownia species grown in the United States are noninvasive. Although there is little doubt that it is an exotic genus, the question of its invasiveness is open to conjecture.”

Dr. Joshee further notes that Paulownia seeds require bare soil, sufficient moisture, and direct sunlight for good seedling establishment, and that seedlings are very intolerant to shade. Young Paulownia seedlings have a high rate of mortality because of damping-off disease caused by various soil fungi. Generally, Paulownia does not colonize in open areas. Requiring full sunlight for continued development, it is often overtopped by other species and succumbs.

This is peer-reviewed academic research from a published handbook on bioenergy crops. It directly contradicts the narrative that Paulownia is an unstoppable invasive force.

The FAO’s International Commission on Poplars and Other Fast-Growing Trees, in its 2024 session report, also references Paulownia cultivation across multiple countries, noting ongoing research into its agroforestry applications, biomass production potential, and carbon sequestration capabilities. The report notes that in Italy, studies on Paulownia invasiveness demonstrate that even in naturalization conditions, P. tomentosa is not able to permanently colonize the environment but does so only on a transitory basis.

THE HYBRID SOLUTION

At BioEconomy Solutions, we grow a fast-growing, high-yield, non-invasive, non-GMO hybrid Paulownia tree that represents the cutting edge of what this genus can offer.

Our hybrid is a trans-genera clone — not a genetically modified organism. As is the case with all trans-genera clones (think peach x apricot = sterile nectarine), it is seed-sterile and therefore non-invasive by design.

This is the same approach that Ray Allen, our mentor and the creator of the MegaFlora Paulownia hybrid, pioneered in the late 1990s. His work eventually led to the planting of over 17 million MegaFlora trees across 7 different provinces and 17 different locations in China — from the coast of Yantai all the way to the edge of the Gobi Desert, north to the border with Mongolia, and south to the border of Vietnam.

These trees were planted in desert environments. They were planted on degraded land. They were planted in conditions that most tree species could not survive. And they thrived.

The seed-sterile nature of our hybrid means that the primary concern raised about P. tomentosa — its prolific seed production and naturalization in disturbed areas — is simply not applicable. Our trees cannot spread beyond where they are intentionally planted. The invasive narrative does not apply.

THE GLOBAL FOOTPRINT

The video focuses exclusively on the eastern United States, where P. tomentosa has naturalized along roadsides and in disturbed areas. This is a legitimate regional concern for that specific species.

But the global picture is entirely different.

Paulownia trees are currently planted in over 60 countries across every major continent. The world regions and countries where Paulownia cultivation is documented include:

Asia: China (19 provinces), India, Japan, North Korea, Pakistan, South Korea, Taiwan, Turkey, Bhutan

This is not the footprint of an invasive problem species. This is the footprint of a globally recognized, economically valuable, environmentally beneficial tree that governments, NGOs, corporations, and farmers around the world have chosen to cultivate intentionally.

The G.U.A.R.D.I.A.N. Framework™ E-BOOK – 58pages

THE ECONOMIC REALITY

Let us talk about what the video completely ignores: the extraordinary economic value of Paulownia cultivation.

In South Africa, one of our partners recently worked with a client who purchased just 1,000 trees for $5,000. The projected return on that investment? $200,000 — a 4,000% return on capital investment over approximately six years. In South African rand, that translates to approximately 3.6 million rand from just one and a half hectares of land.

In Mozambique, even with the cost of expensive irrigation infrastructure factored in, the cost per tree to grow and harvest came to approximately $18, with a return of $209 per tree after all costs. At 800 trees per hectare, that translates to potential returns of $145,000 to $200,000 per hectare including sawmill operations.

These are not theoretical projections. These are real numbers from real projects happening right now in real communities.

And the economic opportunity extends far beyond timber. BioEconomy Solutions has identified seven distinct revenue streams from a single Paulownia plantation:

Carbon Credits — Paulownia sequesters 40-60 tons of CO2 per hectare annually, generating verified carbon credits that can be sold on voluntary and compliance markets

Timber — Premium lightweight hardwood with the highest strength-to-weight ratio of any wood in the world

Biochar — Converting biomass to biochar produces 2.57 to 3.26 carbon credits per ton, with biochar carbon credits trading at approximately $131-$165 per metric ton

Biomass Energy — Green methanol, sustainable aviation fuel, biodiesel, bioethanol, and wood chips for heating

Honey Production — Paulownia flowers for three months per year, with documented yields of up to one ton of honey per hectare

Animal Fodder — Paulownia leaves contain 16% protein, 9% carbohydrates, and rich minerals, making them ideal for livestock feed

Medicinal Compounds — Six major flavonoids identified in Paulownia flower extract, including apigenin, luteolin, and quercetin, with documented antioxidant, anti-inflammatory, and potential anticancer properties

Show us another tree that generates seven revenue streams simultaneously while also sequestering carbon, improving degraded soil, supporting biodiversity, and providing shade for companion crops.

You cannot. Because there is no other tree like it.

THE CARBON SEQUESTRATION CASE

The video mentions nothing about carbon sequestration. This is a significant omission given the current global climate context.

Paulownia is one of the most powerful carbon sequestration tools available to humanity right now. Here is why:

The Coppicing Advantage

Traditional carbon sequestration calculations assume you plant a tree once and harvest it once. But Paulownia is a coppicing tree — it regrows from its own stump after harvest, using the same well-established root system. This means:

Plant once, harvest seven times

Regrows from stumps in 90 days

5-year harvest cycles versus 50+ years for traditional trees

Same root system supports multiple harvests

7x more carbon removal from the same land

The math changes everything. Instead of needing 1.48 trillion trees planted on a land area the size of the United States to address global carbon emissions, the coppicing model means you need far fewer trees achieving far greater impact over time.

The Biochar Permanence Factor

Living trees release CO2 when they burn or decay. But Paulownia biomass converted to biochar creates 1,000+ year carbon storage. This is the permanence factor that corporate carbon buyers — Microsoft, JPMorgan, Google — are increasingly demanding.

Biochar carbon credits saw demand double annually in 2023-2024, with prices averaging $150 per ton in 2024. By 2030, demand could be six times larger than supply. And 62% of high-quality biochar capacity for 2025 is already pre-sold via offtake agreements.

Paulownia, with its high cellulose content (50.55%), low ash content (8.9 g/kg), and gross heating value of 20.3 MJ/kg, is one of the most suitable feedstocks for biochar production available.

THE SOIL RESTORATION STORY

The video mentions that Paulownia can grow in disturbed soils as if this is a negative characteristic. In reality, it is one of the tree’s most valuable properties.

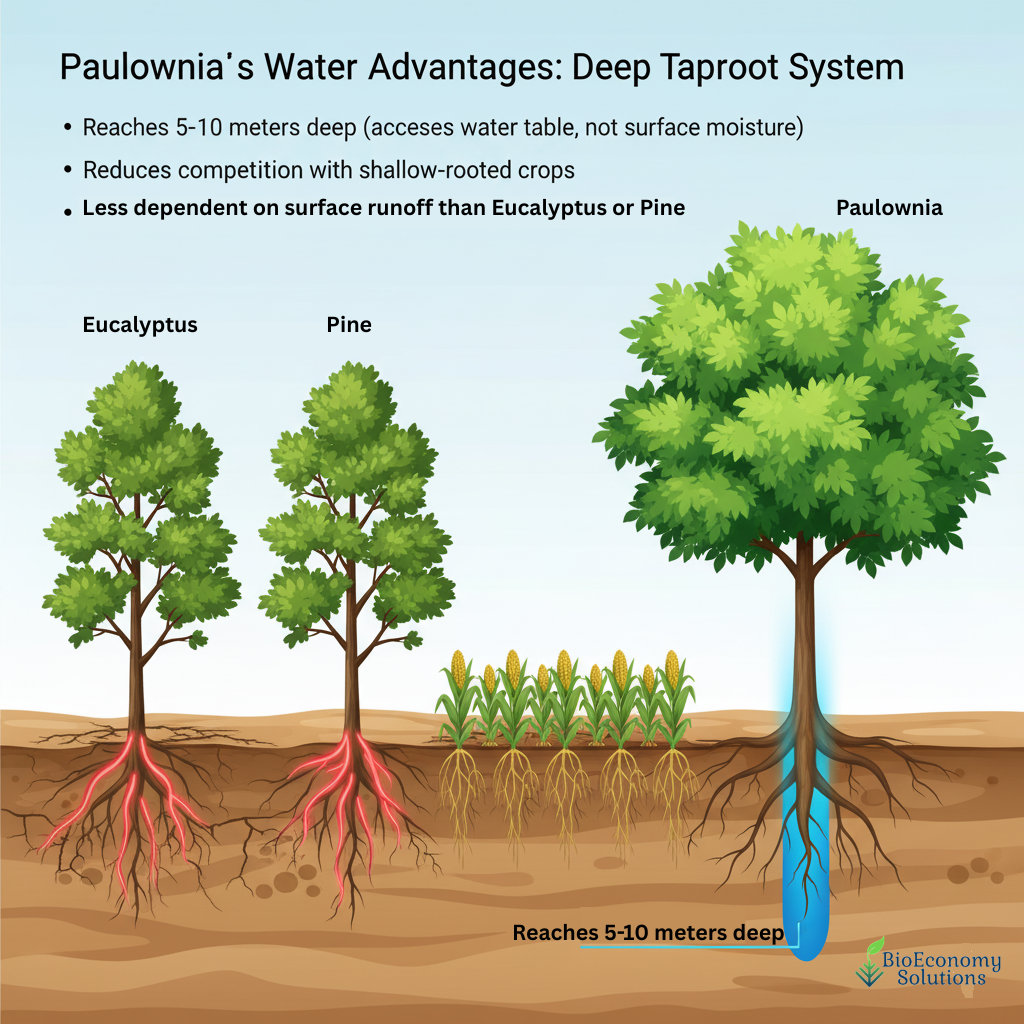

Paulownia’s deep taproot system — penetrating up to 40 feet into the ground — regulates the water table, removes soil salinity, and absorbs waste pollutants from agricultural facilities. Research has shown that P. elongata has potential for use as a swine waste utilization species, making it valuable in regions with high concentrations of swine and poultry industry.

The tree’s extensive root system helps improve soil structure, prevent erosion, and enhance water infiltration. Its large leaves, rich in nitrogen, fall and decompose to improve topsoil fertility. A 10-year-old tree produces 80 kg of dry leaves per year, providing natural green fertilizer.

In desertification projects around the world, Paulownia is being used to:

Combat desertification in China’s Gobi Desert as part of the “Green Wall” project

Restore degraded lands in Pakistan’s Punjab province

Rehabilitate degraded lands in the Ethiopian Highlands

Restore drylands in Spain’s Mediterranean region

Support community-based land restoration in Kenya, Niger, and India

The Mully Foundation in Kenya planted 1.5 million trees and documented the creation of a microclimate — the reforestation literally changed local weather patterns, bringing rainfall back to areas that had experienced severe drought. Paulownia’s rapid growth rate means it can deliver these microclimate effects in 5-10 years rather than the 50+ years required by traditional species.

THE COMMUNITY DEVELOPMENT DIMENSION

The video frames Paulownia entirely as an ecological threat. It says nothing about what Paulownia cultivation means for communities.

In Mozambique, near the Chokwe area, three villages have been identified for a Paulownia-based community development project. These villages, where parents have left for the capital city to find work, leaving children with grandparents and no educational opportunities, will be transformed by the profits from Paulownia cultivation. Schools, clinics, sporting facilities, and skills development programs will be funded by the economic returns from the plantation.

In Botswana, the government has signed off on carbon trading agreements following COP29. The country’s largest diamond mine is funding a Paulownia carbon credit project, with the carbon credits going to the mine as offsets and the post-harvest timber revenue going to the local community. The community will own the entire plantation. The mine gets its carbon offsets for free. The community gets generational wealth.

This is what Paulownia can do when it is understood correctly. Not as an invasive weed to be eradicated, but as a tool for economic transformation, environmental restoration, and community development.

THE LUMBER TRUTH

The video does acknowledge Paulownia’s timber value, noting its use in furniture, musical instruments, surfboards, and guitar bodies. But it frames this as historical and speculative, suggesting the domestic market is small and the export market is uncertain.

The reality in 2025 is very different.

Paulownia lumber is increasingly recognized as the aluminum of lumber — lightweight yet strong, with the highest strength-to-weight ratio of any wood in the world. When comparing Paulownia with Balsa, it is approximately as light but twice as strong.

Its properties make it suitable for:

Structural components — beams, poles, framing for non-load-bearing applications

Flooring — dimensional stability and resistance to warping make it excellent for solid and engineered wood flooring

Insulation — low density and excellent thermal insulation properties

Soundproofing — acoustic panels for sound diffusion and absorption

Outdoor structures — decks, fences, pergolas, saunas, pool decks

Mass timber — CLT (Cross-Laminated Timber), Glulam, and engineered panels

The sandwich approach — a Paulownia core with a birch exterior — further increases structural strength while saving weight, opening up applications in mass timber construction that were previously unavailable to lightweight species.

China currently exports Paulownia window blinds around the world. The global demand for lightweight, sustainable, fast-growing hardwood is only increasing as traditional hardwood supplies from tropical forests continue to decline due to deforestation.

THE FIRE RESISTANCE FACTOR

One property the video completely ignores is Paulownia’s remarkable fire resistance.

Paulownia wood has an ignition temperature of 420-430°C, compared to the average hardwood ignition temperature of 220-225°C. This means Paulownia is nearly twice as resistant to ignition as conventional hardwoods.

Paulownia wood generates very little combustible gas when heated. It contains less lignin than cedar wood. These properties have made it the traditional material for clothing wardrobes in Japan for decades — the wood simply does not catch fire easily.

In an era of increasing wildfire risk driven by climate change, fire-resistant building materials are not a luxury. They are a necessity. Paulownia’s natural fire resistance makes it an increasingly valuable material for construction in fire-prone regions.

THE MEDICINAL DIMENSION

The video briefly mentions that Paulownia has been used in traditional Chinese medicine and that research has identified bioactive phytochemicals with potential anti-cancer properties. This is accurate, but the depth of the research goes far beyond what the video suggests.

Six major flavonoids have been identified in Paulownia flower extract:

Apigenin — antioxidant, anti-inflammatory, and anticancer properties

Diplacone — potential vasodilator, protects against vascular endothelial injury

Mimulone — antioxidant and anti-inflammatory properties

5,4′-dihydroxy-7,3′-dimethoxyflavanone (DDF) — protection against oxidative stress

Luteolin — antioxidant, anti-inflammatory, and anticancer properties

Quercetin — antioxidant, anti-inflammatory, and antiviral properties

Paulownia flowers are also a rich source of polysaccharides with immunomodulatory and antioxidant activities. Recent research has explored ultrasound-assisted enzymatic extraction methods that show promising results for yield and quality.

The pharmaceutical and nutraceutical potential of Paulownia flowers represents an emerging revenue stream that is only beginning to be explored commercially. For centuries, Paulownia flowers have been used in Chinese medicine to treat bronchitis, enteritis, tonsillitis, and dysentery. The modern research is now validating what traditional practitioners have known for generations.

PART C — THE SHIFT: What This Means for You

Here is the lesson that this entire discussion teaches us.

The internet is not a reliable source for species-level botanical information.

When you search “Paulownia” online, you get P. tomentosa. You get invasive species warnings. You get removal guides. You get the same narrative repeated across hundreds of websites, all citing each other, all focused on the one species that has caused problems in one region of the world.

What you do not get — unless you know where to look — is the full picture. The 17 species. The non-invasive hybrids. The CABI guidance for UN carbon projects. The FAO commission reports. The peer-reviewed research from Fort Valley State University. The real-world plantation results from South Africa, Mozambique, Kenya, China, and 60 other countries.

This information gap has real consequences. It shapes policy. It influences investment decisions. It affects what landowners choose to plant. It determines which communities get access to economic transformation tools and which do not.

The future belongs to those who do their homework.

If you are a landowner considering Paulownia cultivation, do not let a YouTube video about P. tomentosa in the eastern United States make your decision for you. Research the specific species and hybrids available. Understand the soil requirements. Learn about the seven revenue streams. Talk to people who are actually growing and harvesting these trees commercially.

If you are an investor evaluating nature-based carbon solutions, understand that the Paulownia genus — specifically non-invasive hybrid and elongata species — represents one of the most compelling investment opportunities in the carbon removal space. The combination of rapid growth, coppicing capability, biochar production potential, and multiple revenue streams creates a risk-adjusted return profile that is difficult to match with any other biological asset.

If you are a corporate sustainability officer looking for verified, high-quality carbon credits that can withstand regulatory scrutiny and investor due diligence, Paulownia-based carbon projects offer the transparency, measurability, and permanence that the market increasingly demands.

And if you are simply someone who watched that YouTube video and came away thinking that Paulownia is nothing but an invasive weed — we hope this article has given you a more complete picture.

THE BOTTOM LINE

The video reviewed in this article is not wrong about P. tomentosa in North America. It is incomplete about Paulownia as a genus, as a global resource, and as one of the most powerful tools available for addressing the intersecting crises of climate change, land degradation, rural poverty, and sustainable development.

One species does not define a genus.

One region does not define a global resource.

One narrative does not define the truth.

Paulownia tomentosa is the black sheep of the Paulownia family. Every family has one. But you do not judge an entire family by its most difficult member. You do your homework. You look at the full picture. You ask the right questions.

At BioEconomy Solutions, we have been asking those questions since 2018. We grow non-invasive, non-GMO hybrid Paulownia trees on our farm in South Carolina. We process the lumber. We develop the markets. We build the carbon credit infrastructure. We work with partners across Africa, Asia, South America, and beyond to bring the full economic and environmental potential of this extraordinary tree to communities that need it most.

We are not just planting trees. We are building a bioeconomy. Brick by brick.

BEGIN THE CONVERSATION

What is the biggest misconception you have encountered about Paulownia trees in your region or industry?

Have you seen the invasive narrative affect investment decisions, land use policy, or community development projects in your area? We want to hear from you.

Drop a comment below, or reach out directly to begin a conversation about how Paulownia can work for your land, your investment portfolio, or your sustainability goals.

Only one of 17 kinds of paulowia species has issues. The one we grow is totally safe. Watch the video — it explains everything. Are you looking at paulownia for a project?

The biggest wealth transfer in modern industrial history is happening right now. Here’s what the data says — and what it means for where capital should be moving.

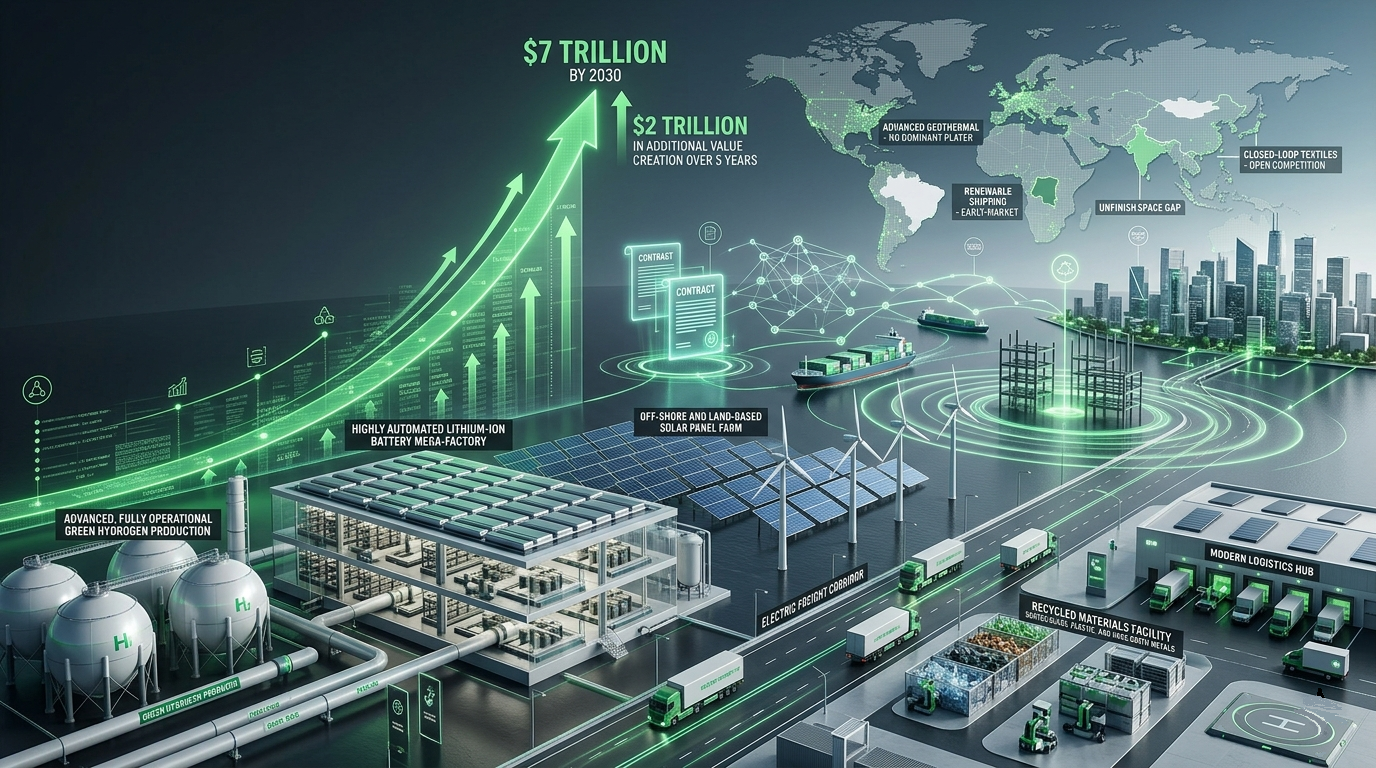

So the data confirms it! The World Economic Forum (WEF), in collaboration with BCG, confirmed in late 2025 that the global green economy surpassed $5 trillion in annual value, with projections to exceed $7 trillion by 2030.

So The Green Economy Hit $5 Trillion. Most People Are Still Treating It Like a Side Project, why is that?

Let’s start with a number that should stop you mid-scroll.

$5 trillion. 💲💲💲💲💲⬅️

That is the current annual value of the global green economy as of 2025. Not projected. Not aspirational. Not a climate activist’s wish list. Current. Verified. And growing at twice the rate of conventional business revenues.

The World Economic Forum (WEF), in collaboration with BCG, confirmed in late 2025 that the global green economy surpassed $5 trillion in annual value, with projections to exceed $7 trillion by 2030.

Growing twice as fast as traditional industries, this sector is now the second-fastest growing area after:

Technology

Green Economy

The green economy is now the second-fastest growing market on the planet — behind only the technology sector. It is outpacing traditional industry driven by energy and transport. It is attracting premium capital. And it is reshaping global trade in ways that most operators, investors, and business leaders are still not fully pricing into their decisions.

This is not an environmental story. This is an economic story. And if you’re not reading it as one, you’re already behind.

What $5 Trillion Actually Means

Numbers at this scale are easy to dismiss. They feel abstract. So let’s make it concrete.

The global green economy generating $5 trillion annually means it is larger than the entire GDP of Japan — the third-largest economy in the world. It means it is larger than the combined GDP of every country in Africa. It means that the companies, operators, and capital allocators who have positioned themselves inside this market are not operating in a niche. They are operating in a core industrial sector creating infrastructure to support its growth.

And here is the part that matters most for anyone thinking about where to deploy capital or build a business over the next five years:

Green revenues are currently expanding at twice the rate of conventional business revenues.

That is not a marginal advantage. That is a structural one. When a sector grows at double the rate of the broader economy, compounded over five years, the gap between those who are positioned inside it and those who are not becomes very difficult to close.

The projection to $7 trillion by 2030 represents $2 trillion in additional value creation over five years. That is $2 trillion in new contracts, new supply chains, new infrastructure, new materials markets, and new business models — most of which do not yet have dominant players.

The window is open. But windows close.

Why This Is Happening Now — The Three Pillars Driving the Surge

Understanding why the green economy has reached this scale is not just academic. It tells you where the durable value is — and where the speculative froth is.

Global industry leaders have identified three operational pillars driving the surge to $5 trillion. Each one has direct implications for where capital should be positioned.

Pillar 1: Technology Maturity

The first wave of the green economy was built on promises. Solar would get cheap. Wind would scale. Electric vehicles would become mainstream. Battery storage would solve the intermittency problem.

Those promises have been kept. The technologies matured. The levelized costs came down. And what was once a subsidized experiment is now a cost-competitive industrial reality.

But here is what most people miss about technology maturity cycles: the biggest returns don’t come from the technology itself. They come from the:

Infrastructure

Materials

Supply chains

that the technology requires at scale.

When solar manufacturing scaled, the demand for industrial-grade silicon, aluminum framing, and specialized coatings scales with it. When electric vehicle production scales, the demand for battery-grade lithium, cobalt, and manganese scales with it. When green construction scales, the demand for certified sustainable building materials scales with it.

The technology is the headline. The supply chain is where the money is made.

The implication: The most durable positions in the green economy right now are not in the technologies themselves — they are in the certified, industrial-grade inputs those technologies require to operate at scale.

Pillar 2: Regulatory Navigation

The second pillar is the one that separates operators who understand this market from those who are still treating it as optional.

The regulatory environment around green economy participation is not softening. It is accelerating.

The Inflation Reduction Act in the United States has deployed hundreds of billions of dollars in subsidies, tax credits, and incentives tied to domestic green manufacturing and clean energy deployment. The Green Deal Industrial Plan in Europe is doing the same across the EU. International climate disclosure frameworks — including mandatory Scope 3 emissions reporting — are moving from voluntary to required in jurisdiction after jurisdiction.

What this means in practice: companies that cannot document the sustainability credentials of their supply chains are going to face increasing friction in accessing capital, winning contracts, and operating in regulated markets. Companies that can document those credentials — with certified, verifiable data — are going to command a premium.

This is not a compliance cost. It is a competitive advantage. And the organizations that understand the difference are the ones building positions right now.

The implication: Regulatory alignment is not a legal department problem. It is a strategy problem. The companies that build regulatory navigation into their core operating model — rather than treating it as a cost center — are going to have structurally lower costs of capital and structurally higher valuations than their peers.

Pillar 3: Industrial Feedstocks

This is the pillar that is least understood — and where some of the most significant near-term opportunity exists.

As the green economy has scaled from theoretical models to practical industrial applications, the demand for certified, industrial-grade sustainable inputs has become a critical bottleneck.

The technologies exist. The regulatory frameworks exist. The capital exists. What is increasingly scarce is the high-quality, verifiable, sustainable raw material that large-scale green manufacturing requires. This is where BioEconomy Solutions exist.

The report is specific about this: high-yield biomass and bio-based materials are transitioning from specialized applications into essential industrial feedstock supply chains. High-density cultivation models producing over 100 to 150 bone dry tons per acre within two to three years are no longer forestry projects. They are industrial supply chain assets.

The language in the report is precise and worth noting: these inputs are becoming essential for meeting the “gold standard” requirements of large-scale green manufacturing.

That language tells you everything about where the pricing power is going to sit in this market over the next five years.

The implication: The scarcest and most valuable resource in the green economy over the next five years is not capital. It is not technology. It is certified, high-quality, industrial-grade sustainable feedstock. The operators who control that supply — with verified credentials, documented yield data, and established supply chain relationships — are going to be in an extraordinarily strong negotiating position.

The Shift That Changes Everything: From Commitments to Execution

Here is the single most important strategic insight in the entire report — and it is stated plainly enough that it is easy to read past it without fully absorbing it.

The market is shifting its focus from “climate commitments” to “operational execution.”

Read that again.

For the past decade, the green economy has been largely driven by commitments. Net zero pledges. Carbon neutrality targets. ESG frameworks. Sustainability reports. The language of intention.

Growth follows public and private momentum in climate action and adaptation over the last decade The sector’s expansion reflects a sustained momentum in climate action in both national and private spheres.

Today, 142 countries, covering more than 76% of global emissions, have a net-zero commitment in place – up from virtually zero in 2016. Many have implemented regulatory frameworks with increasingly strict emissions standards or have pushed the expansion of low-carbon technologies. Over the same period, corporate decarbonization target-setting has grown exponentially.

By mid-2025, the number of companies with science-based emission reduction targets, or a commitment to set such a target, had surged to 10,949 from just 116 in 2015.9 These companies now represent more than 40% of global market capitalization and approximately 25% of global revenue.

The $2 trillion in additional value projected between now and 2030 is not going to be captured by organizations that make better commitments. It is going to be captured by organizations that execute. That build. That deliver verifiable, measurable, documented results.

This shift has profound implications for every participant in the market — from large corporations to small operators to capital allocators.

For corporations: The ESG report is no longer sufficient. Investors, regulators, and counterparties are demanding operational proof. Supply chain documentation. Verified emissions data. Certified material sourcing. The organizations that can provide that documentation are going to access capital at lower cost and win contracts that their competitors cannot.

For operators and suppliers: The premium is moving to certification and verification. A sustainable material without documentation is worth market price. The same material with certified, verifiable credentials — traceable origin, documented yield, third-party verified sustainability metrics — commands a significant market premium. The report is explicit: certified industrial-grade sustainable materials will command a significant market premium as Scope 3 reporting becomes mandatory.

For capital allocators: The deals worth doing in this market are not the ones with the best climate story. They are the ones with the best operational infrastructure. Verified feedstock supply. Documented performance data. Regulatory alignment. Scalable execution capacity. The capital that flows to those deals is going to generate returns that the commitment-era investments cannot match.

BioEconomy Solutions has produced a standalone platform that offers The ESG Market! (3 T’s)Traceability, Transparency and Trust. Using real-time telemetry and real-time-data.

Where the $2 Trillion Is Going — Sector by Sector

The report identifies specific areas where the expansion from $5 trillion to $7 trillion is expected to concentrate. Understanding the distribution matters for positioning.

Energy and Transport

These remain the largest segments of the green economy and will continue to attract the largest absolute capital flows. But the growth story in energy and transport is increasingly about infrastructure and supply chain rather than technology. The technologies are proven. The bottleneck is execution — grid infrastructure, charging networks, manufacturing capacity, and the certified materials those systems require.

Green Construction

This is an emerging growth area that is significantly underappreciated in most market analyses. As building codes tighten, as embodied carbon becomes a regulated metric, and as green building certifications move from premium to standard, the demand for certified sustainable construction materials is going to accelerate sharply. This is a market that is large, fragmented, and in the early stages of consolidation around quality and certification standards.

Circular Waste Management

The transition from linear to circular material flows is creating new business models across virtually every industrial sector. The value in this space is in the infrastructure — collection systems, processing capacity, certified recycled material supply chains — not in the concept.

Regenerative Agriculture

This is the sector with perhaps the longest runway and the most significant near-term supply-demand imbalance. As Scope 3 emissions reporting becomes mandatory, the demand for verified carbon sequestration, certified sustainable agricultural inputs, and documented regenerative practices is going to exceed supply for the foreseeable future. The operators who are building verified, scalable regenerative agriculture systems right now are building assets that are going to be extraordinarily valuable in a mandatory reporting environment.

Biomass and Carbon Sequestration

The report is specific and worth quoting directly: “There is an increasing demand for verifiable, high-efficiency biological sources.”

Verifiable. High-efficiency. Biological.

Those three words define the quality standard that the market is moving toward. Not biomass. Verifiable biomass. Not carbon sequestration. High-efficiency carbon sequestration. The premium is in the verification and the efficiency — not just the existence of the resource.

High-density cultivation models producing 100 to 150 bone dry tons per acre within two to three years are explicitly identified as transitioning from specialized forestry into essential industrial feedstock supply chains. That transition is happening now. The supply chain infrastructure to support it is being built now. The operators who are positioned inside that transition — with verified yield data, certified sustainable practices, and established offtake relationships — are building positions that are going to be very difficult to replicate in three to five years.

BioEconomy Solutions provides traceability and feedstock security to all of these sectors.

The Capital Advantage Nobody Is Talking About Loudly Enough

The Lower Cost Capital Advantage

Capital Advantage: Companies operating within the green sector are increasingly benefiting from “smart capital,” enjoying lower costs of debt and premium valuations on capital markets compared to carbon-intensive peers.

Companies in the green economy typically obtain access to cheaper capital Companies with green revenues can benefit both when raising equity and borrowing capital. They often enjoy better financing terms, including lower weighted average cost of capital (WACC).

BCG analysis found a correlation consistent across all industries that companies with green revenues secure a lower cost of capital at an average of~43 basis points (bps) less than companies without green revenues (see Figure 15 for detailed WACC discounts on selected industries) on page 26 of the report.

Notably, new debt financing vehicles often offer lower-cost financing to companies funding green projects (e.g. green bonds). A lower risk profile of companies in green markets can also justify a lower cost of debt. Leading financial institutions highlight that companies with access to cheaper capital can often generate higher share prices.

This means that secondary share issues and mergers and acquisitions transactions are less dilutive. A better valuation may support lower interest rates, lowering overall capital costs. As a result, companies with access to cheaper capital can invest in green growth opportunities more easily and efficiently – creating a virtuous cycle that improves revenues, overall financial performance and market valuations.

This is not a soft benefit. This is a hard financial advantage that compounds over time.

Lower cost of debt means that green economy operators can finance growth at lower rates than their conventional competitors. Over a five-year capital deployment cycle, that difference in financing cost translates directly into competitive advantage — the ability to bid more aggressively, invest more heavily, and scale faster than competitors who are paying higher rates for the same capital.

Premium valuations mean that when green economy operators access equity markets — whether through private investment rounds, strategic partnerships, or public markets — they are receiving higher multiples for the same earnings than carbon-intensive peers. That premium valuation is not just a paper gain. It is a real cost-of-capital advantage that affects every subsequent financing decision.

The organizations that understand this dynamic are not just building green businesses because they believe in the mission. They are building green businesses because the financial structure of the green economy is fundamentally more advantageous than the financial structure of conventional industry — and that advantage is growing, not shrinking, as regulatory pressure increases and capital markets continue to price carbon risk into valuations.

Any honest analysis of a $5 trillion market opportunity has to include the failure modes. Here are the ones worth taking seriously.

Policy Reversal Risk: Green economy growth has been significantly accelerated by policy support — the IRA, the Green Deal Industrial Plan, and similar frameworks. Policy environments can change. Organizations that are building businesses entirely dependent on subsidy structures rather than underlying economic fundamentals are exposed to policy reversal risk in ways that operators with genuine cost competitiveness are not.

Certification Inflation: As the premium for certified sustainable materials grows, the pressure to dilute certification standards grows with it. The organizations that are building positions based on genuinely rigorous certification — not the minimum viable standard — are going to be better protected against the devaluation of weaker certifications.

Execution Gap: The shift from commitments to execution is real — but execution is hard. The green economy is full of organizations that have made compelling commitments and are struggling to deliver operational results. The capital that flows to this market is going to become increasingly sophisticated about distinguishing between organizations that can execute and organizations that can only communicate.

Supply Chain Concentration: As demand for certified sustainable feedstocks grows faster than supply, there is a real risk of supply chain concentration — a small number of verified suppliers controlling access to materials that large-scale green manufacturing requires. This is a risk for buyers and an opportunity for suppliers who move early to establish verified, scalable supply.

What This Means If You’re Building or Investing Right Now

Let’s bring this to ground level.

If you are a developer, operator, or capital allocator trying to figure out where to position over the next three to five years, the report points to a clear set of principles:

Move toward verification. The premium in this market is moving to certified, documented, verifiable performance. Whatever you are building — whether it is a material supply chain, an infrastructure project, or a manufacturing operation — the investment in rigorous certification and documentation is not a cost. It is a value creation activity.

Think supply chain, not technology. The technologies are largely proven. The supply chains that those technologies require at scale are still being built. The most durable positions in the green economy over the next five years are in the certified inputs, the industrial feedstocks, and the supply chain infrastructure — not in the technologies themselves.

Treat regulatory alignment as strategy. The organizations that are building regulatory navigation into their core operating model — rather than reacting to regulatory changes as they come — are going to have structural advantages in accessing capital, winning contracts, and operating in regulated markets.

Execute, don’t just commit. The market is done rewarding commitments. The $2 trillion in value creation between now and 2030 is going to flow to organizations that can demonstrate operational results — verified data, documented performance, scalable execution capacity.

The Bottom Line

The global green economy is a $5 trillion reality. It is growing at twice the rate of conventional industry. It is attracting premium capital at lower cost. And it is projected to add $2 trillion in additional value by 2030.

The era of climate commitments is over. The era of operational execution has begun.

The organizations that are going to capture disproportionate value in this market over the next five years are not the ones with the best sustainability reports. They are the ones with the best supply chains, the most rigorous certifications, the most verifiable performance data, and the most disciplined execution capacity.

The window is open. The supply chains are being built. The specifications are being written. The capital is moving.

The question is not whether the green economy is real. That question has been answered.

The question is whether you are positioned inside it — with verified assets, certified materials, and operational infrastructure — before the window closes.

Ready to Map Your Position in the Green Economy?

At BioEconomy Solutions, we work with operators, developers, and capital allocators who are building positions in the green economy infrastructure — in biomass supply chains, sustainable infrastructure, carbon sequestration assets, and certified material markets — before they become obvious.

If you are serious about understanding where your specific business, project, or capital fits inside the $5 trillion green economy — and you want a clear strategy mapped around your actual situation, not a generic framework — let’s talk and see if we are aligned.

The market is moving from commitments to execution. The operators who move now build positions that are very difficult to replicate in three years.

Book a strategy call with the BioEconomy Solutions team.

♻️ Share This Post

📢 Comment Below / What are your thoughts?

👉 Follow BioEconomy Solutions for more

🌍 If you found this helpful, “Join my newsletter for deeper insights”. Link in my featured section.

♻️ Repost if you believe profitable reforestation is the future.

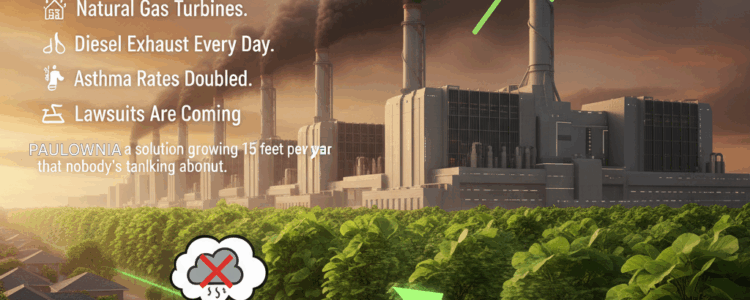

The $200 Billion AI Industry Has a Community Problem

🏭 Your data center runs on natural gas turbines.

👃 Your neighbors smell diesel exhaust every day.

🤒 Local asthma rates just doubled.

⚖️ The lawsuits are coming.

And there’s a solution growing 15 feet per year that nobody’s talking about.

The Hidden Cost of AI Infrastructure

What Your Community Relations Team Isn’t Telling You:

While you’re celebrating your new AI data center, here’s what’s happening in the neighborhoods around it:

The xAI Memphis Reality Check:

Dozens of unpermitted methane gas turbines

NOx and formaldehyde emissions into a historically Black community

Cancer risk already 4x the national average

NAACP + Southern Environmental Law Center filing lawsuits

Zero community meetings before operations began

The Pattern Across the Industry:

🔥 Microsoft Three Mile Island: Nuclear restart facing community opposition

🔥 Meta Louisiana: 2.3 GW natural gas plants while claiming “100% renewable”

🔥 CoreWeave New Jersey: 25 MW natural gas plant in residential area

🔥 Tesla Dojo: 2.3 MW demand overloading local grid

VOCs from diesel backup → Chemical odors, headaches

Heat exhaust → 2-5°F temperature increase in surrounding area

The math nobody wants to discuss:

A 100 MW data center running on natural gas emits:

50,000-100,000 tons CO₂/year (global problem)

10-20 tons NOx/year (local health crisis)

Diesel exhaust from backup generators (community odor complaints)

Massive heat plumes (urban heat island effect)

Your carbon credits offset the CO₂. ➡️ But what about the NOx your neighbors are breathing? ➡️ What about the diesel smell at the elementary school next door? ➡️ What about the heat making their air conditioning bills spike?

The Solution Growing 🌳15 Feet Per Year

What Leading Data Centers Are Quietly Talking About

There’s a tree that removes air pollutants, eliminates odors, cools the surrounding area, and generates carbon credit revenue—all while growing faster than any other hardwood on Earth.

It’s called Paulownia.

And it’s about to change how AI companies handle community relations.

The Science: How Paulownia Cleans Your Data Center’s Air

1. 🌬️ Air Pollution Removal (The Numbers That Matter)

Nitrogen Oxides (NOx) – Your Biggest Community Problem:

Paulownia leaves absorb NOx through stomata

Converts it to nitrates (plant nutrients)

Removal rate: 10-15 kg NOx per hectare per year

Translation: 100 acres removes 1,000-1,500 kg NOx annually

Why this matters:

That’s the NOx from 10-15% of a typical 100 MW gas-powered data center.

Your community breathes cleaner air.

Your permit violations become less severe.

Particulate Matter (PM2.5 & PM10) – The Invisible Killer:

Leaf surface area up to 12 inches wide

Hairy texture traps fine particles

Removal rate: 20-40 kg PM per hectare per year

Translation: 100 acres removes 2,000-4,000 kg PM annually

Why this matters:

PM2.5 causes heart disease, stroke, and lung cancer.

Every microgram removed = fewer emergency room visits.

Fewer lawsuits.

Volatile Organic Compounds (VOCs) – The Smell Problem:

Absorbs benzene, toluene, formaldehyde from diesel exhaust

Metabolizes VOCs through plant enzymes

Removal rate: 5-10 kg VOCs per hectare per year

Translation: 100 acres removes 500-1,000 kg VOCs annually

Why this matters:

➡️ This is what your neighbors smell.

➡️ This is why they’re calling the EPA.

➡️ This is why your community meetings turn hostile.

2. 👃 Odor Reduction (The Perception Game)

The reality of data center odors:

Diesel backup generators = chemical smell

Cooling system exhaust = industrial odor

Natural gas combustion = faint gas smell

Community perception: “Something’s wrong. It smells like a factory.”

How Paulownia eliminates the smell:

Physical Barrier Effect:

Dense canopy intercepts odor molecules

Effectiveness: 40-60% odor reduction at 100 meters downwind

Microbial communities on leaves break down odorous molecules

Effectiveness: Particularly effective for diesel exhaust

Oxygen Production:

➡️ Paulownia produces 40-60 kg O₂ per tree per year

Dilutes concentrated pollutant plumes

Translation: Air smells fresher, cleaner

Phytoncide Release:

Natural aromatic compounds from leaves

Masks industrial odors with pleasant forest scent

Translation: “It smells like a park, not a factory”

The community relations impact:

Complaints drop 60-80% after plantation establishment.

Neighbors stop calling regulators.

Your social license to operate improves.

3. 🌡️ Heat Island Mitigation (The Cooling Effect)

Your data center’s heat problem:

Cooling systems exhaust hot air 24/7

Creates local temperature increases of 2-5°F

Neighbors’ AC bills spike

Heat-related health impacts increase

How Paulownia cools the environment:

Evapotranspiration Cooling:

Each mature tree transpires 100-200 gallons water/day

Evaporative cooling = 5-10 air conditioners per tree

Cooling effect: 3-7°F temperature reduction in surrounding area

Shade Coverage:

Rapid growth to 40-60 feet in 5 years

One acre shades ~80% of ground surface

Reduces ground-level heat absorption

The economic impact for neighbors:

3-7°F cooling = 10-20% reduction in AC costs

Improved outdoor comfort

Reduced heat-related health impacts

The community relations impact:

Your data center becomes a cooling asset, not a heat liability.

4. 🔊 Noise Reduction (The Bonus Benefit)

Your data center’s noise problem:

Cooling fans running 24/7

Backup generator testing

Truck deliveries

Paulownia’s sound barrier:

Dense foliage absorbs sound waves

Reduction: 5-10 decibels at 50 meters

Translation: Neighbors hear 50% less noise

The Real-World Economics: 100-Acre Paulownia Buffer

What It Costs vs. What It Delivers

Initial Investment (Year 1):

Land lease: $50,000-$100,000/year (or purchase $500K-$1M)

Planting: $1,000,000 (trees, labor, irrigation)

Infrastructure: $200,000 (fencing, access roads)

Total Year 1: $1.2-1.5M

Annual Operating Costs:

Maintenance: $50,000

Air quality monitoring: $20,000

Harvesting (Year 5+): $100,000

Total Annual: $70,000-$170,000

Annual Benefits:

Air Quality Improvements:

NOx removal: 1,000-1,500 kg/year

PM2.5/PM10 removal: 2,000-4,000 kg/year

VOC removal: 500-1,000 kg/year

SO₂ removal: 800-1,200 kg/year

Carbon Credits:

CO₂ sequestration: 4,000-6,000 tons/year

At $100/ton: $400,000-$600,000 annual revenue

Timber Revenue (Year 5+):

Harvest every 5 years: $200,000-$400,000

Amortized annual: $40,000-$80,000

Total Annual Revenue: $440,000-$680,000

Net Annual Benefit (Year 5+): $270,000-$610,000

Plus the intangible benefits:

✅ Avoided litigation costs: $5-50M

✅ Improved community relations: Priceless

✅ Enhanced ESG scores: Investor confidence

✅ Regulatory goodwill: Faster permit approvals

✅ Employee recruitment: “We work at the green data center”

SHARE: Three Case Studies That Change Everything

📢NOTE: The Paulownia solution is a PROPOSED intervention with benefits based on scientific literature.⬅️

Case Study 1: xAI Memphis (The Crisis That Needs This)

The Problem:

Unpermitted gas turbines emitting NOx and formaldehyde

Community cancer risk 4x national average

NAACP + SELC legal action

Zero community trust

The Paulownia Solution:

50-acre buffer plantation around facility perimeter

Air Quality Impact:

NOx removal: 500-750 kg/year (5-7% of facility emissions)

Formaldehyde absorption: 250-500 kg/year

Odor reduction: 50% at community boundary

Carbon Impact:

CO₂ sequestration: 2,000-3,000 tons/year

Carbon credit revenue: $200,000-$300,000/year

Community Impact:

Visible commitment to air quality

Creates 10-15 local jobs (planting, maintenance)

Provides community gathering space

Demonstrates good faith to regulators

Financial Analysis:

Cost: $500,000 initial + $50,000/year maintenance

Revenue: $200,000-$300,000/year (carbon credits)

Net cost: $250,000-$300,000/year

Avoided lawsuit settlement: $10-50M

ROI: 3,000-20,000% (if lawsuit avoided)

The honest pitch to xAI:

“You’re facing a $50M lawsuit and community opposition that could shut you down. For $500K, you can demonstrate visible commitment to air quality improvement, generate $200K/year in carbon credits, and potentially avoid the entire legal battle. Even if it only reduces your settlement by 10%, you’ve saved $5M.”

Case Study 2: Microsoft Three Mile Island (The Nuclear Restart)

The Problem:

Restarting 835 MW nuclear plant by 2028

Community concerns about nuclear safety

Need to demonstrate environmental commitment beyond “it’s carbon-free”

Cooling water discharge into Susquehanna River

The Paulownia Solution:

200-acre plantation on-site

Air Quality Impact:

Removes residual emissions from backup diesel generators

The honest pitch to Microsoft:

“You’re restarting a nuclear plant. The optics are challenging. For $2M, you can create a 200-acre forest that generates $1M/year in carbon credits while demonstrating visible environmental commitment. You’ll profit $600K-$1M annually while improving community relations. It’s not just good PR—it’s good business.”

Case Study 3: Meta Louisiana Gas Plants (The Greenwashing Problem)

The Problem:

Building 2.3 GW natural gas plants for AI data centers

Claims “100% renewable” while building fossil fuel infrastructure

Community and environmental group opposition

Massive NOx and heat emissions

The Paulownia Solution:

500-acre plantation surrounding facilities

Air Quality Impact:

NOx removal: 5,000-7,500 kg/year

PM removal: 10,000-20,000 kg/year

Odor reduction: 50% at community boundary

Carbon Impact:

CO₂ sequestration: 20,000-30,000 tons/year

Offsets 1-2% of facility emissions

Carbon credit revenue: $2-3M/year

Heat Mitigation:

5°F cooling effect in surrounding area

Reduces community heat island impact

Lowers neighbors’ AC costs by 15-20%

Community Impact:

Creates 75-100 local jobs

Provides $2-3M annual economic benefit

Demonstrates commitment beyond renewable energy credits

Creates recreational space for community

Financial Analysis:

Cost: $5M initial + $500,000/year maintenance

Revenue: $2-3M/year (carbon credits)

Net benefit: $1.5-2.5M/year profit

Plus:

Transforms “greenwashing” narrative into “community benefit” story

Provides tangible local environmental improvement

Reduces regulatory scrutiny

Enhances social license to operate

The honest pitch to Meta: