From Dirt to Dollars: How BioEconomy Solutions Is Quietly Building the Infrastructure That Powers the Green Economy

The Three Pillars Nobody Is Talking About — Renewable Energy, Agro-Industrial Agriculture, and Waste Management

Most green energy companies sell you a vision.

BioEconomy Solutions builds the infrastructure that makes it real.

While the world debates climate policy, carbon markets, and net-zero targets, a quiet revolution is happening in the fields, farms, and waste streams of communities across four continents.

It does not make headlines.

It does not trend on social media.

But it is the foundation upon which every credible sustainability strategy must eventually be built.

Three sectors sit at the heart of this revolution:

- Renewable Energy and Power.

- Agro-Industrial Agriculture Infrastructure.

- Waste Management — collection, transportation, and treatment.

Most companies pick one. They go deep on solar. Or they focus on sustainable agriculture. Or they build waste processing facilities.

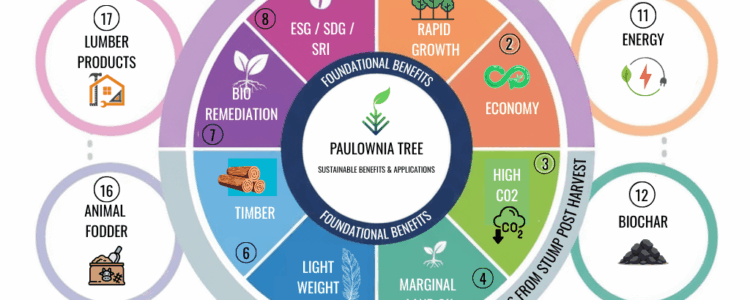

BioEconomy Solutions does all three. Simultaneously. From the same biological asset. Using the same fast-growing, non-invasive, non-GMO hybrid BES Paulownia Carbon Orchards, trees that has been planted in over 60 countries and is now at the center of the most exciting convergence in the history of sustainable development.

This is not a coincidence. This is a system.

And in this article, we are going to show you exactly how it works.

PART A — STAKES: Why These Three Sectors Are the Most Important Investments of the Next Decade

Before we get into the specifics of what BioEconomy Solutions does and how we do it, let us establish why these three sectors matter so much right now.

The Renewable Energy Gap

The global energy transition is the defining economic story of our time. Governments around the world have committed to net-zero carbon emissions by 2050. The International Civil Aviation Organization has set a goal of reducing aviation emissions by 5% by 2030. The European Union has mandated that 2% of all aviation fuel must be sustainable by 2025, rising to 70% by 2050.

These are not aspirational targets. They are regulatory requirements with financial penalties for non-compliance.

And yet the infrastructure to meet these targets does not fully exist yet.

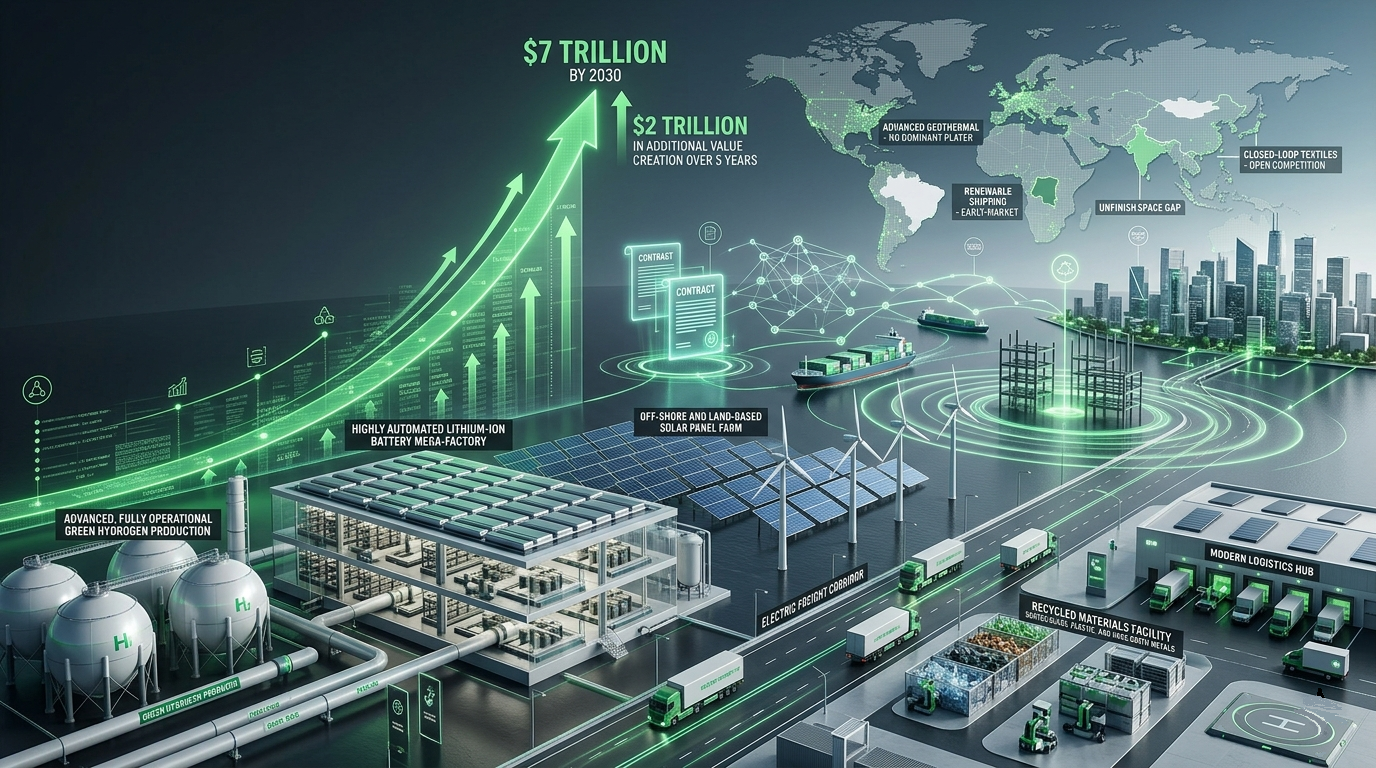

The gap between where we are and where we need to be represents one of the largest investment opportunities in human history. Bloomberg New Energy Finance estimates that the global energy transition will require $173 trillion in investment between now and 2050. The renewable energy sector alone is projected to grow from its current scale to become the dominant form of energy production globally within the next two decades.

For BioEconomy Solutions, this gap is not a problem. It is an opportunity.

BES Carbon Orchards biomass — woody chips, pellets, biochar, green methanol, sustainable aviation fuel, biodiesel, and bioethanol — represents a renewable energy feedstock that can be produced at scale, on degraded land, in communities that need economic development, with a carbon footprint that is negative rather than positive.

This is not theoretical. This is happening right now.

The Agro-Industrial Infrastructure Deficit

Agriculture feeds the world. But the infrastructure that connects farms to markets, raw materials to processing facilities, and biological assets to financial value is chronically underdeveloped — especially in the regions where agricultural potential is greatest.

Sub-Saharan Africa loses an estimated $4 billion per year in post-harvest agricultural losses due to inadequate infrastructure. South Asia loses a similar amount. Latin America faces comparable challenges.

The problem is not the land. The land is there. The problem is not the farmers. The farmers are there. The problem is the infrastructure — the roads, the processing facilities, the storage systems, the logistics networks, the quality control systems, the certification frameworks — that transforms raw agricultural potential into realized economic value.

Agro-industrial infrastructure is the missing link between agricultural abundance and economic prosperity. And it is the sector that receives the least attention from mainstream investors, despite offering some of the most compelling risk-adjusted returns available in the developing world.

BioEconomy Solutions focuses specifically on the infrastructure components of agro-industrial projects. Not just the farming. Not just the processing. The entire system — from soil preparation and seedling production through harvest, processing, certification, and market access.

This systems approach is what separates a successful agro-industrial project from a failed one. And it is what BioEconomy Solutions brings to every project we engage with.

The Waste Management Crisis

The world produces approximately 2.01 billion tonnes of municipal solid waste annually. By 2050, that figure is projected to reach 3.4 billion tonnes. In low and middle income countries, over 90% of waste is disposed of in unregulated dumps or open burning sites.

The environmental consequences are severe. Open burning of waste is a significant source of greenhouse gas emissions, toxic air pollutants, and soil and water contamination. Unmanaged waste streams contribute to disease, reduce agricultural productivity, and undermine the quality of life in communities that are already facing significant development challenges.

But here is what most people miss about waste management.

Waste is not a problem. Waste is a resource that has not yet been properly managed.

Agricultural residues, municipal solid waste, used cooking oil, animal waste, crop waste — all of these waste streams contain enormous amounts of embedded energy, nutrients, and biological value that can be captured and converted into economic assets.

Biochar from agricultural waste. Green methanol from woody biomass. Biogas from organic waste. Compost from crop residues. Carbon credits from waste-to-energy projects. These are not futuristic technologies. They are proven, commercially viable processes that are being deployed right now by forward-thinking companies and governments around the world.

BioEconomy Solutions sits at the intersection of all three of these sectors. And the BES Carbon Orchards tree is the biological engine that powers the entire system.

PART B — THE STORY: How BioEconomy Solutions Builds the Green Economy Infrastructure

PILLAR ONE: RENEWABLE ENERGY AND POWER

The BES Carbon Orchards Energy Platform

When most people think about renewable energy, they think about solar panels and wind turbines. These are important technologies. But they have limitations — intermittency, land use requirements, grid integration challenges, and the inability to produce liquid fuels for transportation.

Biomass energy from fast-growing tree plantations addresses many of these limitations. It is dispatchable — meaning it can be produced on demand rather than depending on weather conditions. It can be converted into liquid fuels for transportation, aviation, and shipping. It can be used for heat and power generation. And when managed sustainably, it is carbon neutral or even carbon negative.

BES Carbon Orchards is the ideal biomass energy crop for several reasons.

First, the growth rate. BES Carbon Orchards trees can grow up to 10-15 feet per year, making them one of the fastest-growing trees in the world. A plantation established today can be harvested in as little as three to five years, providing a rapid return on investment that is simply not possible with slower-growing species.

Second, the yield. Research conducted at the World BES Carbon Orchards Institute suggests that up to 100 bone dry tons of fiber per acre per year can be produced by establishing a BES Carbon Orchards farm. This is a biomass yield that rivals or exceeds most dedicated energy crops, including switchgrass, miscanthus, and short-rotation willow.

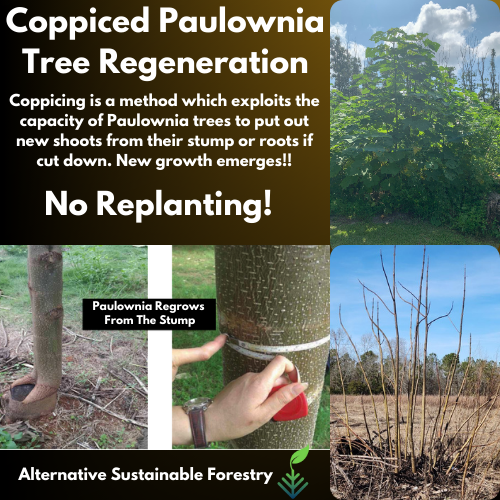

Third, the coppicing advantage. After harvest, BES Carbon Orchards regrows from its own stump using the same well-established root system. This means the plantation does not need to be replanted after each harvest. The same trees can be harvested up to seven times, dramatically reducing the cost per ton of biomass produced over the life of the plantation.

Fourth, the energy content. BES Carbon Orchards wood has a gross heating value of 20.3 MJ/kg, which is comparable to or higher than most other hardwood species. Its cellulose content of 50.55% makes it an excellent feedstock for biochemical conversion processes. Its low ash content (8.9 g/kg) and low sulphur content (0.00%) make it a clean-burning fuel with minimal emissions.

The Renewable Energy Products

From a single BES Carbon Orchards plantation, BioEconomy Solutions can produce multiple renewable energy products:

Biochar

Biochar is produced by heating BES Carbon Orchards biomass in a controlled, low-oxygen environment through a process called pyrolysis. The resulting material is a stable, carbon-rich substance that can be used as a soil amendment, a carbon sequestration tool, and a source of verified carbon credits.

Wood feedstocks like BES Carbon Orchards produce between 2.57 and 3.26 carbon credits per ton of biochar, with an average of 2.83 credits per ton. In 2023, the price of biochar carbon credits reached $131 per metric ton, and prices have continued to rise as corporate demand for high-quality, permanent carbon removal credits increases.

The permanence of biochar carbon storage — 1,000+ years — is what makes it particularly valuable to corporate buyers who need to demonstrate genuine, long-term carbon removal rather than temporary sequestration that could be reversed by fire, disease, or deforestation.

Green Methanol

Green methanol from BES Carbon Orchards woody biomass is produced through a gasification process that converts the biomass into synthesis gas (syngas), which is then converted into methanol through catalytic synthesis.

Green methanol is increasingly recognized as a critical fuel for the maritime shipping industry, which is under enormous pressure to decarbonize. The International Maritime Organization has set targets for significant emissions reductions from shipping by 2030 and 2050, and green methanol is one of the most promising pathways to meet those targets.

BES Carbon Orchards’s high cellulose content and rapid growth rate make it an ideal feedstock for green methanol production. The process is carbon neutral because the CO2 released during combustion is offset by the CO2 absorbed during the tree’s growth cycle.

Sustainable Aviation Fuel

The Kenya Business Implementation Study commissioned by ICAO identifies sustainable aviation fuel as one of the most critical needs in the global energy transition. Kenya alone imports approximately 1.2 million cubic meters of jet fuel annually, and the country has committed to reducing aviation emissions by 5% by 2030.

BES Carbon Orchards biomass can be converted to sustainable aviation fuel through multiple pathways, including gasification followed by Fischer-Tropsch synthesis, alcohol-to-jet conversion, and direct biomass-to-liquid processes. The tree’s high biomass yield, rapid growth rate, and ability to grow on marginal land make it an ideal feedstock for SAF production in regions like East Africa where land is available but conventional feedstocks are limited.

Biodiesel and Bioethanol

Research has demonstrated that bioethanol production from BES Carbon Orchards biomass achieves 100% ethanol conversion in selected conditions, with an energy recovery of 97.5%. This makes BES Carbon Orchards one of the most efficient cellulosic ethanol feedstocks available.

Biodiesel production from BES Carbon Orchards is also possible through the transesterification of oils extracted from the tree’s seeds and biomass. Rudolf Diesel himself envisioned vegetable oil as the fuel of the future when he demonstrated his engine running on peanut oil at the 1900 World’s Fair. BES Carbon Orchards is helping to fulfill that vision more than a century later.

Wood Chips and Pellets

For markets where liquid fuel conversion is not yet economically viable, BES Carbon Orchards biomass can be processed into wood chips and pellets for use in biomass heating and power generation systems. European and Asian markets have strong demand for sustainably sourced wood pellets, and BES Carbon Orchard’s rapid growth rate and high yield make it a cost-competitive supplier.

Forage harvesters normally used to process corn and other crops are now employed to efficiently cut, chip, and load BES Carbon Orchards wood fiber at production levels of 80-100 green tons per hour. This mechanized harvesting capability makes large-scale biomass production economically viable in a way that was not possible with manual harvesting methods.

PILLAR TWO: AGRO-INDUSTRIAL AGRICULTURE INFRASTRUCTURE

The Infrastructure Gap

The difference between a successful agro-industrial project and a failed one is almost never the biology. The trees grow. The crops produce. The yields are there.

The difference is the infrastructure.

Infrastructure in the context of agro-industrial projects means:

- Nursery and propagation facilities — producing high-quality, disease-free planting stock at scale

- Soil preparation and land management systems — ensuring optimal growing conditions from day one

- Irrigation infrastructure — providing reliable water supply in regions where rainfall is insufficient or unreliable

- Harvest and processing equipment — converting standing biomass into marketable products efficiently

- Storage and logistics systems — moving products from farm to market without loss or degradation

- Quality control and certification frameworks — ensuring products meet the standards required by buyers

- Carbon measurement and verification systems — documenting and verifying carbon sequestration for credit generation

- Market access and offtake agreements — connecting production to buyers who will pay fair prices

BioEconomy Solutions focuses specifically on these infrastructure components because they are where most agro-industrial projects fail. A beautiful plantation with no processing facility is worthless. A processing facility with no reliable feedstock supply is equally worthless. The infrastructure must be designed as an integrated system from the beginning.

The Micropropagation Foundation

Every successful BES Carbon Orchards agro-industrial project begins with high-quality planting stock. BioEconomy Solutions operates micropropagation laboratories that produce tissue-cultured BES Carbon Orchards seedlings with consistent genetic characteristics, disease resistance, and growth performance.

Micropropagation — the production of plants through tissue culture rather than seeds or cuttings — offers several critical advantages for agro-industrial projects:

- Genetic consistency — every plant is genetically identical to the parent, ensuring predictable growth rates, timber quality, and biomass yield

- Disease freedom — tissue-cultured plants are produced in sterile conditions, eliminating the risk of introducing soil-borne diseases to new planting sites

- Scalability — tissue culture facilities can produce millions of plants per year from a small number of parent plants

- Non-invasive characteristics — our hybrid BES Carbon Orchards is seed-sterile, meaning it cannot spread beyond where it is intentionally planted

Our micropropagation facility in South Africa serves projects across the African continent, providing the foundation for agro-industrial BES Carbon Orchards projects from Mozambique to Kenya to Botswana to Burkina Faso.

The Agri-Hub Model

The most effective model for agro-industrial BES Carbon Orchards development is the agri-hub — a centralized facility that serves as the hub of a regional feedstock supply chain.

An agri-hub typically includes:

- A nursery and propagation facility producing planting stock for the surrounding region

- A training center providing farmers with the knowledge and skills to grow BES Carbon Orchards successfully

- A primary processing facility for initial biomass processing — chipping, drying, pelletizing

- A quality control laboratory for testing biomass quality and certifying products for sale

- A logistics hub for aggregating biomass from multiple farms and coordinating transportation to processing facilities

- A carbon measurement station for monitoring and verifying carbon sequestration across the plantation network

This model has been proven by Eni’s agri-hub operations in Kenya, which have worked with over 100,000 smallholder farmers across 11 counties and achieved the first Low Indirect Land Use Change certification in Kenya under the International Sustainability and Carbon Certification scheme.

BioEconomy Solutions is building a similar agri-hub network across Africa, with facilities in South Africa, Mozambique, and planned expansions into Kenya, Uganda, Botswana, and beyond.

The Intercropping Advantage

One of the most powerful features of BES Carbon Orchards as an agro-industrial crop is its compatibility with intercropping — the practice of growing other crops between the rows of trees.

BES Carbon Orchards’s deep taproot system — penetrating up to 40 feet into the ground — does not compete with the shallow roots of most agricultural crops. Its large leaves provide shade that can benefit shade-tolerant crops while its canopy reduces wind speed by 20-50%, protecting companion crops from wind damage.

Intercropping options that work well with BES Carbon Orchards include:

- Soybeans — nitrogen-fixing legumes that improve soil fertility while providing a cash crop

- Groundnuts — sun-loving crops that thrive in the open spaces between young BES Carbon Orchards trees

- Ginger — a high-value spice crop that benefits from the microclimate created by BES Carbon Orchards

- Winter wheat and millet — staple food crops that benefit from wind protection and improved soil moisture

- Fodder crops — grasses and legumes for livestock feed that benefit from the shade and soil improvement provided by BES Carbon Orchards

- Cut flowers — high-value horticultural crops that can be grown between tree rows for additional income

The intercropping model transforms a BES Carbon Orchards plantation from a single-product investment into a diversified agricultural enterprise that generates income from multiple sources simultaneously. This diversification reduces risk, improves cash flow during the years before the first timber harvest, and creates more employment opportunities for local communities.

The Soil Restoration Infrastructure

BES Carbon Orchards is not just a crop. It is a soil restoration tool.

In regions where land has been degraded by overgrazing, deforestation, erosion, or industrial contamination, BES Carbon Orchards can be used to restore soil health while simultaneously generating economic returns.

The tree’s deep taproot system breaks up compacted soil layers, improving water infiltration and aeration. Its fallen leaves decompose to add organic matter and nutrients to the topsoil. Its root system stabilizes slopes and prevents erosion. Its canopy reduces evaporation and moderates soil temperature.

Research has shown that BES Carbon Orchards roots penetrate down as far as 40 feet, regulating the water table and removing soil salinity. BES Carbon Orchards trees have been shown to be very effective in absorbing waste pollutants from hog, chicken, and dairy facilities as well as various other pollutants.

For agro-industrial projects on degraded land — which represents the majority of available land in many developing regions — this soil restoration capability is not just an environmental benefit. It is an economic one. Improved soil health means higher crop yields, lower input costs, and greater long-term productivity from the land.

People ask me this all the time.

“Where do I go to learn about the Trillion Dollar Green Economy?”

I always say the same thing.

Go here: https://www.youtube.com/@BioEconomySolutions2

The Carbon Infrastructure

The carbon measurement, reporting, and verification infrastructure that BioEconomy Solutions deploys across its agro-industrial projects is what transforms a tree plantation into a verified carbon asset.

Our Net Eco Exchange platform uses satellite monitoring, Internet of Things sensors, and blockchain technology to provide real-time tracking of carbon sequestration down to the soil level. This data infrastructure enables:

- Real-time carbon accounting — continuous monitoring of CO2 sequestration across the plantation

- Third-party verification — independent audit of carbon claims by recognized certification bodies

- Blockchain tokenization — conversion of verified carbon credits into digital tokens that can be traded on carbon markets

- ESG reporting integration — direct connection to corporate ESG reporting platforms including CDP, GRI, and SASB

- Double-counting prevention — blockchain-based tracking ensures each carbon credit is counted only once

This infrastructure is what corporate buyers of carbon credits increasingly demand. The era of unverified, untracked carbon offsets is ending. The future belongs to projects that can demonstrate real, measurable, permanent carbon removal with transparent, auditable data.

BioEconomy Solutions is building that infrastructure today.

PILLAR THREE: WASTE MANAGEMENT — COLLECTION, TRANSPORTATION, AND TREATMENT

Waste as a Resource

The conventional view of waste management is that it is a cost — a necessary expense that communities and businesses must bear to maintain public health and environmental quality.

BioEconomy Solutions takes a fundamentally different view.

Waste is a resource. Every ton of agricultural residue, municipal solid waste, used cooking oil, animal waste, or crop byproduct that is currently being burned, dumped, or left to decompose represents embedded energy, nutrients, and biological value that can be captured and converted into economic assets.

The circular economy principle — where waste from one process becomes the input for another — is not just an environmental philosophy. It is a business model. And it is a business model that BioEconomy Solutions has built into the core of every project we develop.

Agricultural Waste Streams

A BES Carbon Orchards plantation generates multiple waste streams that can be converted into valuable products:

Harvest Residues

When BES Carbon Orchards trees are harvested for timber, approximately 50% of the tree’s biomass is converted into dimensional lumber. The other 50% — tops, branches, bark, and small-diameter wood — is typically considered waste.

BioEconomy Solutions converts this harvest residue into:

- Biochar — through pyrolysis, generating carbon credits and soil amendment products

- Wood chips — for biomass energy production or sale to industrial users

- Wood pellets — for heating and power generation markets

- Green methanol feedstock — for conversion to liquid fuel

- Animal bedding — processed wood fiber for livestock operations

Nothing is wasted. Every part of the tree has value.

Leaf Biomass

BES Carbon Orchards leaves are rich in protein (16.2%), carbohydrates (9.44%), and minerals, making them ideal for animal fodder and green fertilizer. A 10-year-old tree produces 80 kg of dry leaves per year.

Rather than allowing fallen leaves to decompose unmanaged, BioEconomy Solutions incorporates leaf biomass collection into the plantation management system, either as:

- Direct animal fodder — fed fresh or dried to livestock

- Green fertilizer — incorporated into the soil to improve fertility

- Compost feedstock — combined with other organic materials to produce high-quality compost

Seed and Flower Byproducts

BES Carbon Orchards flowers are a rich source of flavonoids with documented pharmaceutical and nutraceutical value. Rather than treating flowers as waste, BioEconomy Solutions is developing collection and processing systems to capture this value.

BES Carbon Orchards seeds, while not used for propagation in our seed-sterile hybrid varieties, contain oils that can be extracted for industrial applications.

Municipal and Agricultural Waste Integration

Beyond the waste streams generated by BES Carbon Orchards plantations themselves, BioEconomy Solutions integrates municipal and agricultural waste management into its project designs.

Used cooking oil — one of the most valuable waste streams for biofuel production — is collected from restaurants, food processing facilities, and households and converted into biodiesel or used as a feedstock for HEFA-based sustainable aviation fuel production.

Agricultural residues from companion crops grown between BES Carbon Orchards rows — crop stalks, husks, seed pods, and other organic materials — are collected and processed into biochar, compost, or biomass energy feedstock.

Animal waste from livestock operations integrated with BES Carbon Orchards plantations is processed through biogas digesters to produce renewable energy and nutrient-rich digestate for soil amendment.

The Waste-to-Energy Infrastructure

The collection, transportation, and treatment of waste streams requires dedicated infrastructure that most agro-industrial projects do not include in their initial design.

BioEconomy Solutions designs waste management infrastructure as an integral component of every project from the beginning, including:

Collection Systems

- Designated collection points at regular intervals throughout the plantation

- Mechanized collection equipment for harvest residues

- Collection networks for used cooking oil from surrounding communities

- Coordination with municipal waste management authorities for organic waste streams

Transportation Infrastructure

- On-farm road networks designed for heavy equipment access

- Logistics coordination systems for aggregating waste streams from multiple sources

- Cold chain infrastructure for perishable waste streams

- Bulk transport systems for high-volume, low-value waste streams like wood chips

Treatment Facilities

- Pyrolysis units for biochar production from woody biomass

- Biogas digesters for organic waste treatment and energy production

- Composting facilities for nutrient recovery from organic waste

- Oil processing equipment for used cooking oil collection and pre-treatment

- Pelletizing equipment for converting loose biomass into dense, transportable fuel pellets

The Carbon Value of Waste Management

Proper waste management is not just an environmental and economic benefit. It is a carbon benefit.

When agricultural residues are burned in open fields — as happens with an estimated 500 million tons of agricultural residue annually in India alone — they release CO2, methane, and black carbon into the atmosphere. When organic waste decomposes in unmanaged landfills, it produces methane — a greenhouse gas with 80 times the warming potential of CO2 over a 20-year period.

By capturing these waste streams and converting them into biochar, biogas, or other stable products, BioEconomy Solutions prevents the release of these greenhouse gases while simultaneously generating verified carbon credits.

This waste-to-carbon-credit pathway is one of the most compelling value propositions in the carbon market today. It addresses a real environmental problem — unmanaged waste — while generating economic value for the communities that implement it.

Green Economy Hit $5 Trillion. Institutional Capital Still Treating It Like a Side Project

THE INTEGRATED SYSTEM

The true power of BioEconomy Solutions’ approach is not in any one of these three pillars individually. It is in the integration of all three.

A BioEconomy Solutions project is not a renewable energy project that happens to use agricultural land. It is not an agricultural project that happens to produce some energy. It is not a waste management project that happens to generate some carbon credits.

It is an integrated bioeconomy system where:

- The plantation produces timber, biomass, carbon credits, honey, animal fodder, and medicinal compounds

- The energy infrastructure converts biomass into biochar, green methanol, sustainable aviation fuel, biodiesel, and bioethanol

- The waste management system captures every residue stream and converts it into additional value

- The carbon infrastructure measures, verifies, and tokenizes carbon sequestration across the entire system

- The community development model ensures that economic value flows to local farmers, workers, and communities

This integration is what creates the seven revenue streams that BioEconomy Solutions generates from a single BES Carbon Orchards plantation:

- Carbon credits from growing trees

- Premium timber from harvest

- Biochar carbon credits from biomass processing

- Renewable energy products — SAF, green methanol, biodiesel, bioethanol

- Honey from plantation flowers

- Animal fodder from leaves and harvest residues

- Medicinal and nutraceutical compounds from flowers and leaves

No other biological asset generates this breadth of value from a single planting. No other company has built the integrated infrastructure to capture all seven streams simultaneously.

BOOST THE SHARE

THE SHIFT: What This Means for Investors, Landowners, and Communities

The convergence of renewable energy, agro-industrial agriculture, and waste management is not a future trend. It is happening right now.

The companies and investors who recognize this convergence early — who understand that the most valuable assets in the green economy are not solar panels or wind turbines but biological systems that produce energy, sequester carbon, restore soil, manage waste, and create community wealth simultaneously — will be the ones who capture the greatest returns from the energy transition.

BioEconomy Solutions is not waiting for the future. We are building it.

For Investors

The integrated bioeconomy model that BioEconomy Solutions has developed offers a risk-adjusted return profile that is difficult to match in any other asset class. Multiple revenue streams reduce dependence on any single market. The coppicing model reduces capital requirements for replanting. The carbon credit revenue provides a floor price that supports project economics even when commodity prices are volatile. The community development model creates social license and reduces operational risk.

For Landowners

If you have land — degraded land, marginal land, agricultural land that is not performing — BES Carbon Orchards offers a pathway to transform that land into a productive, multi-revenue bioeconomy asset. You do not need perfect soil. You do not need abundant rainfall. You need the right species, the right infrastructure, and the right partner.

For Communities

The agro-industrial infrastructure that BioEconomy Solutions builds does not just create economic value for investors and landowners. It creates jobs, skills, and economic opportunity for the communities where our projects are located. From nursery workers and plantation managers to processing facility operators and logistics coordinators, every BioEconomy Solutions project creates a cascade of employment and economic activity that extends far beyond the plantation fence.

THE BOTTOM LINE

Renewable energy. Agro-industrial agriculture infrastructure. Waste management.

Three sectors. One integrated system. One biological engine.

The BES Carbon Orchards tree is not just a fast-growing hardwood. It is the foundation of a new bioeconomy — one that generates energy, sequesters carbon, restores soil, manages waste, and creates community wealth simultaneously.

BioEconomy Solutions has spent years building the infrastructure, the knowledge, and the partnerships to make this vision a reality. We are not selling a concept. We are delivering results — in South Carolina, in South Africa, in Mozambique, in Botswana, in Kenya, in Togo, in Burkina Faso, and in dozens of other locations across four continents.

The green economy is not coming. It is here.

The question is not whether you will be part of it.

The question is whether you will be part of it early enough to capture the full opportunity.

Are you ready to build something that lasts?

BEGIN THE CONVERSATION

What is the biggest infrastructure gap you see in your region’s transition to renewable energy and sustainable agriculture?

Drop a comment below. We read every one.

Visit us: bioeconomysolutions.com

Book a call: bioeconomysolutions.com/bookcall

Email: mail@bioeconomysolutions.com

Phone: 843.305.4777

♻️ Repost this if you believe the green economy must be built on integrated biological systems — not just solar panels and wind turbines.

Share with an investor, landowner, or sustainability leader who needs to see the full picture.

Tag someone who is building the infrastructure of the future.

#BioEconomy #RenewableEnergy #AgroIndustrial #WasteManagement #BES Carbon Orchards #CarbonCredits #SustainableAgriculture #Biochar #GreenMethanol #SAF #CircularEconomy #ESG #NatureBasedSolutions #AfricaInvestment #RegenerativeAgriculture

BioEconomy Solutions | South Carolina, USA | Serving projects in 60+ countries

© 2025 BioEconomy Solutions. All rights reserved.

The G.U.A.R.D.I.A.N. Framework™ E-BOOK – 58pages

Download your FREE E-Book Copy:

The G.U.A.R.D.I.A.N. Framework™

Growing sustainable biomass at scale

Unifying industry, farmers, and environment

Achieving net-zero operations

Regenerating degraded landscapes

Diversifying rural income streams

Integrating carbon credit economies

Accelerating climate solutions

Nurturing 35+ year supply chains

BioEconomy Solutions (BES) is pioneering the transition from extractive to regenerative industrial operations through The G.U.A.R.D.I.A.N. Framework™ https://bioeconomy-solutions.kit.com/020c5628ce