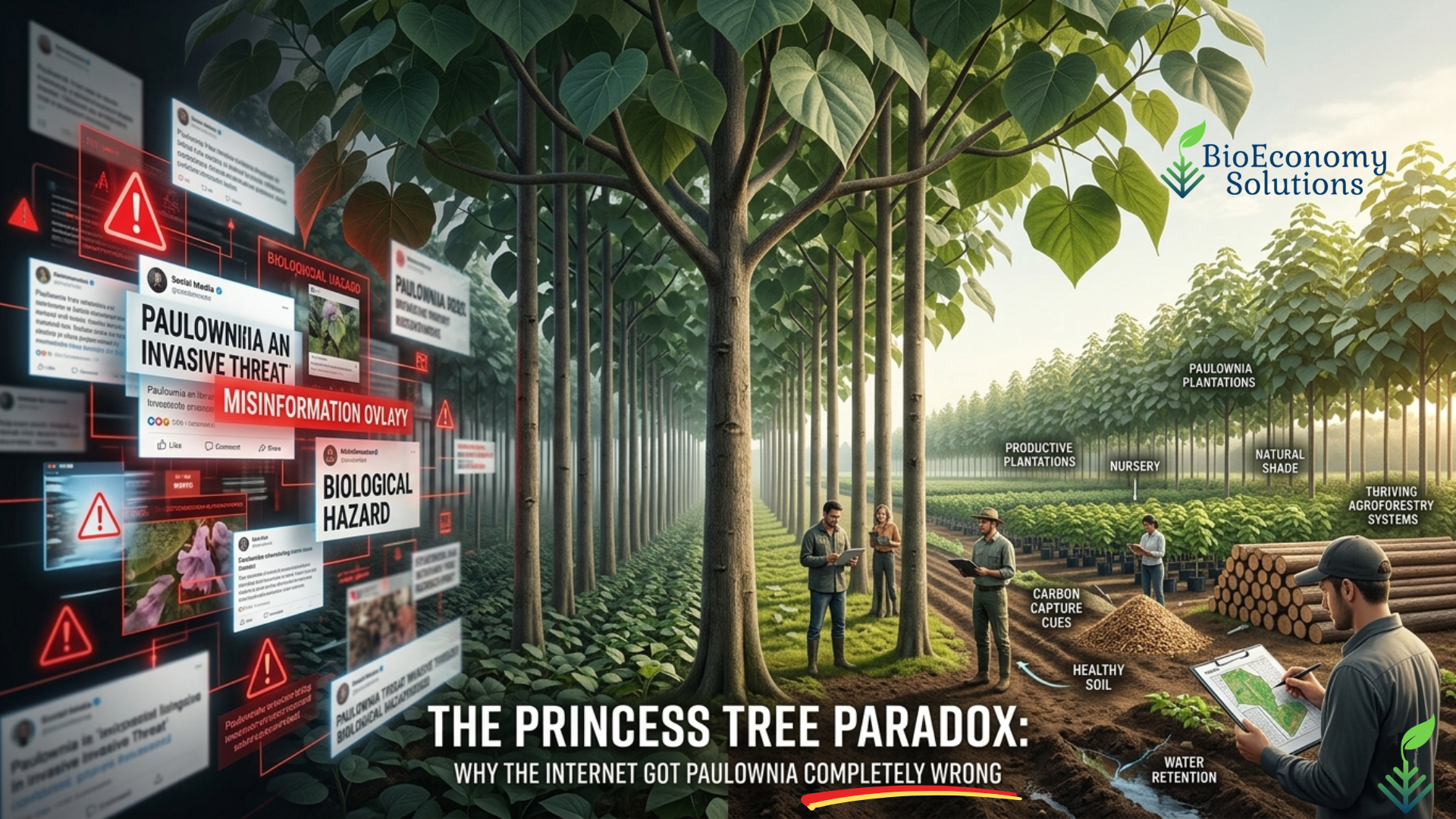

The Princess Tree Paradox: Why the Internet Got Paulownia Completely Wrong

A BioEconomy Solutions Response to the Viral “Invasive Tree” Narrative

The internet just called one of the world’s most valuable trees a villain.

And 99% of people believed it without asking a single question.

A popular YouTube video titled “This Invasive Tree is Named After Russian Royalty!” has been circulating widely, painting the Paulownia tree as an ecological menace — a fast-spreading invader threatening native plant communities across North America. The video is well-produced, the narrator is knowledgeable, and the identification content is genuinely useful.

But here is the problem.

The video talks about one species out of seventeen.

And in doing so, it has contributed to one of the most damaging misconceptions in modern agroforestry, sustainable agriculture, and carbon sequestration science. A misconception that is costing landowners, investors, governments, and communities around the world billions of dollars in missed opportunity.

We are not here to attack the video creator. We are here to set the record straight.

Because when a tree is being planted in over 60 countries, used in United Nations carbon credit plantations, studied by CABI in Wellington, UK, and recognized by the FAO International Commission on Fast-Growing Trees as one of the most promising species for sustainable development — it deserves more than a one-sided narrative built on a single species out of seventeen.

So let us break this down. Brick by brick.

PART A — STAKES: Why This Misconception Costs the World

Before we get into the science, let us establish why this matters beyond a simple YouTube comment section debate.

The global carbon credit market is projected to grow from $8 billion to over $200 billion in the next six years. Nature-based solutions, including fast-growing tree plantations, are at the center of that growth. Corporations with net-zero commitments, governments under Paris Agreement obligations, and institutional investors seeking ESG-compliant assets are all looking for verified, scalable, nature-based carbon removal solutions.

Paulownia — specifically non-invasive hybrid and elongata species — sits at the intersection of every single one of those needs.

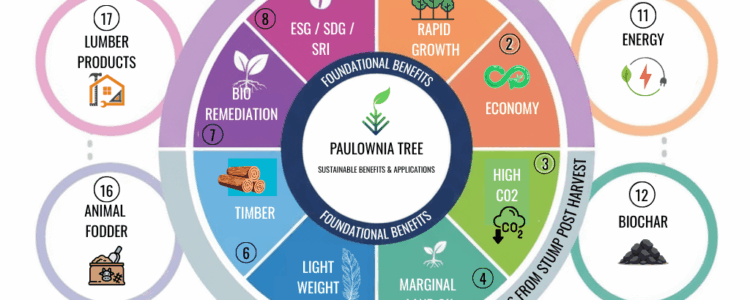

It is one of the fastest-growing hardwood trees on the planet. It sequesters carbon at rates that dwarf most other species. It coppices — meaning it regrows from its own stump after harvest — up to seven times without replanting. It improves degraded soil. It supports biodiversity through intercropping. It produces premium timber, biochar, biomass for green energy, honey, animal fodder, medicinal compounds, and more.

And yet, because of the widespread conflation of P. tomentosa with the entire Paulownia genus, landowners are hesitant to plant it. Investors are cautious about funding it. Regulators in some regions have placed blanket restrictions on it. And the general public, armed with a YouTube video and a Google search that surfaces the same tomentosa-focused content over and over again, dismisses it entirely.

The cost of this misconception is not just financial. It is environmental.

Every year that Paulownia plantations are delayed because of misinformation is another year that degraded land goes unrestored. Another year that carbon stays in the atmosphere. Another year that rural communities in Africa, Asia, South America, and the American South miss out on economic transformation.

That is the real cost of getting this wrong.

Paulownia Tomentosa “BLACK SHEEP” Of Paulownia Family

PART B — THE STORY: What the Video Got Right, and Where It Went Wrong

Let us be fair. The video does several things well.

The identification content for Paulownia tomentosa is accurate and detailed. The narrator correctly describes the heart-shaped leaves, the vanilla-scented purple flowers, the distinctive bark patterns, the hollow chambered pith, and the aggressive stump sprouting behavior. For someone trying to identify and manage P. tomentosa on their property in the eastern United States, this video is genuinely useful.

The historical context is also largely accurate. P. tomentosa was introduced to Europe in the 1830s by the Dutch East India Company. It arrived in North America shortly after, initially for silviculture and ornamental purposes. Its seeds were famously used as natural packing material for glassware shipped from Asia, which contributed to its naturalization across the eastern United States.

The video correctly notes that P. tomentosa can invade disturbed areas, produce enormous quantities of seeds, and regrow aggressively from stumps and roots. In the context of managing this specific species in North American native plant communities, these are legitimate concerns.

But here is where the narrative breaks down.

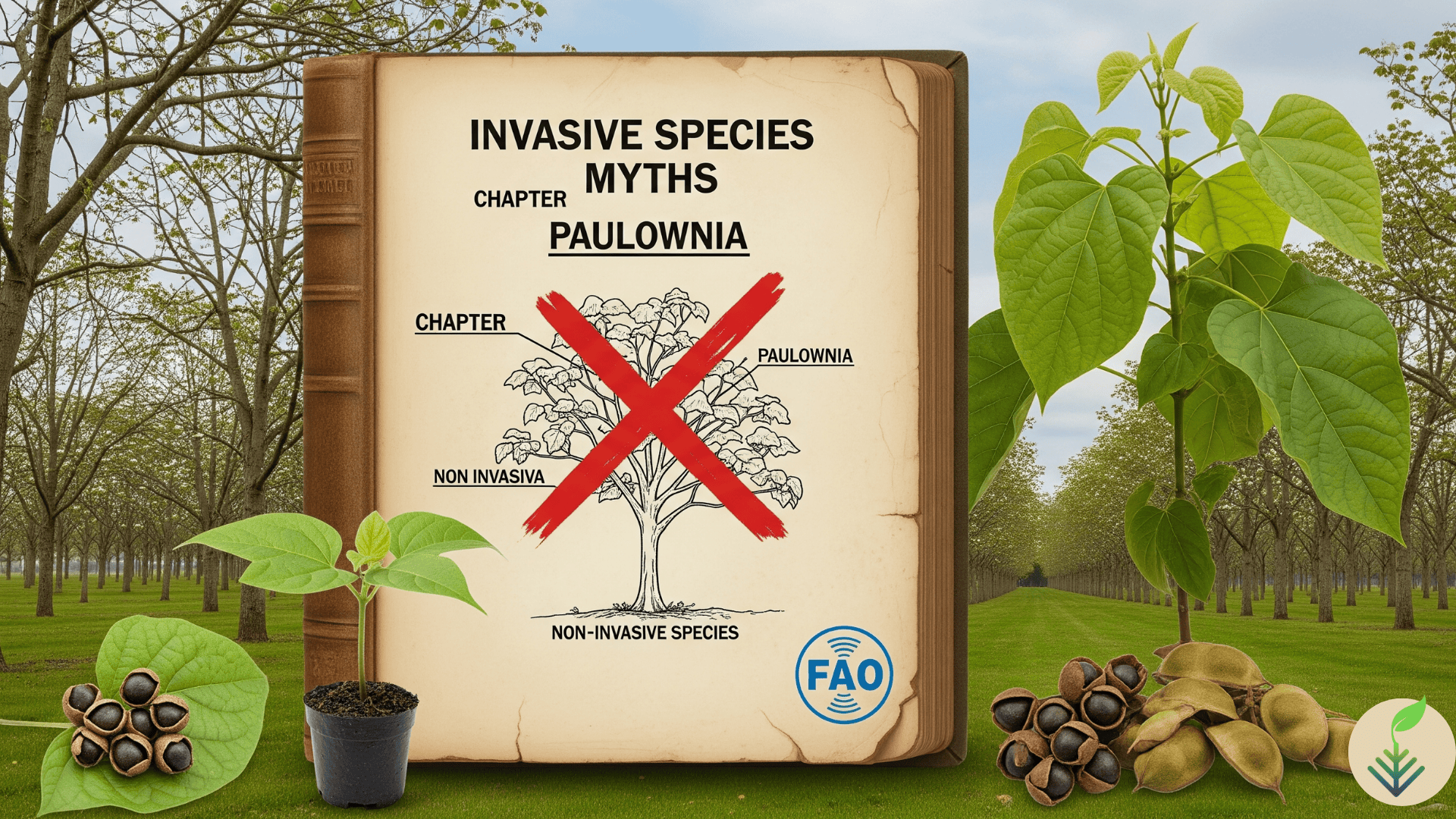

The video never once mentions that there are 17 different species of Paulownia.

Not once.

It never distinguishes between P. tomentosa and P. elongata, P. fortunei, P. kawakamii, or any of the other confirmed species. It never mentions the non-invasive hybrid varieties that have been specifically developed for commercial cultivation. It never references the CABI document prepared for United Nations countries that explicitly accepts P. elongata as a non-invasive species for carbon credit plantations. It never acknowledges that the invasive behavior it describes is largely dependent on the presence of sterile soil — construction sites, burn areas, road cuts — and that Paulownia rarely colonizes open fields because of naturally occurring soil fungi.

Instead, it presents a single species narrative and applies it to the entire genus.

This is the equivalent of saying that because one variety of apple is toxic, all apples should be avoided. Or because one breed of dog is aggressive, all dogs are dangerous. The logic does not hold, and in the case of Paulownia, the consequences of that flawed logic are significant.

THE 17 SPECIES REALITY

Let us be very specific about what the Paulownia genus actually contains.

According to taxonomic authorities, there are between 6 and 17 species of Paulownia in the family Paulowniaceae. The confirmed and tested species include:

- Paulownia kawakamii — native to Taiwan, smaller stature, deep purple flowers

- Paulownia tomentosa — the Princess Tree, the one species listed as invasive in some areas

- Paulownia catalpifolia — slower growing, excellent wood quality

- Paulownia x taiwaniana — natural hybrid between P. fortunei and P. kawakamii

- Paulownia elongata — extremely fast-growing, ideal for intercropping and carbon sequestration

- Paulownia fargesii — valued for timber production

- Paulownia fortunei — the Dragon Tree, native to southeast Asia, rapid growth, tall stature

Additionally, there are numerous potential variety, hybrid, and synonym species including P. glabrata, P. grandifolia, P. imperialis, P. australis, P. lilacina, P. longifolia, P. meridionalis, P. mikado, P. recurva, P. rehderiana, P. shensiensis, P. silvestrii, P. thyrsoidea, P. duclouxii, and P. viscosa.

Of all of these species, only P. tomentosa is listed as invasive in some areas of the world.

The video discusses only P. tomentosa. But the title, framing, and general narrative create the impression that “Paulownia” as a whole is an invasive problem. This is the core of the misinformation.

WHAT CABI ACTUALLY SAYS

The Collaborative International Agricultural Biodiversity Institute (CABI), based in Wellington, UK, prepared a comprehensive compendium on Paulownia specifically for the purpose of identifying the Paulownia elongata species for use in United Nations countries for carbon credit plantations.

This is not a fringe document. This is a globally recognized scientific institution preparing guidance for UN-level carbon development projects.

The document does state that “Paulownia is categorized as an invasive exotic.” And yes, that line exists. But the full context of that statement is critical, and it is worth quoting in full:

“Paulownia is categorized as an invasive exotic. Although there is little doubt that it is an exotic, the question of its invasiveness is open to conjecture. The many small seeds of Paulownia are windblown. However, the seeds do not germinate and survive unless the seed falls on sterile soil. New germinates of Paulownia have a high rate of mortality from damping-off disease caused by a variety of soil fungi. Generally, Paulownia does not colonize open areas unless sterile soil is present, as in construction activities, recent burned areas and road cuts. Rarely does Paulownia colonize fields, because of the ever-present fungi.”

Read that again carefully.

The seeds do not germinate and survive unless they fall on sterile soil. New seedlings have a high rate of mortality from naturally occurring soil fungi. Paulownia rarely colonizes fields because of those fungi.

This is a dramatically different picture from the one painted in the video, where 20 million seeds per year sounds like an unstoppable ecological invasion. The reality is that the vast majority of those seeds never survive to become established trees. The conditions required for successful naturalization are far more specific and limited than the video implies.

And critically, the CABI document accepts P. elongata as a non-invasive species in all United Nations countries for the purpose of carbon credit plantation development.

THE RESEARCH CONFIRMS IT

The academic research on Paulownia is extensive and largely positive. Dr. Nirmal Joshee of Fort Valley State University, whose comprehensive chapter on Paulownia appears in the Handbook of Bioenergy Crop Plants, notes that:

“Except for P. tomentosa, most Paulownia species grown in the United States are noninvasive. Although there is little doubt that it is an exotic genus, the question of its invasiveness is open to conjecture.”

Dr. Joshee further notes that Paulownia seeds require bare soil, sufficient moisture, and direct sunlight for good seedling establishment, and that seedlings are very intolerant to shade. Young Paulownia seedlings have a high rate of mortality because of damping-off disease caused by various soil fungi. Generally, Paulownia does not colonize in open areas. Requiring full sunlight for continued development, it is often overtopped by other species and succumbs.

This is peer-reviewed academic research from a published handbook on bioenergy crops. It directly contradicts the narrative that Paulownia is an unstoppable invasive force.

The FAO’s International Commission on Poplars and Other Fast-Growing Trees, in its 2024 session report, also references Paulownia cultivation across multiple countries, noting ongoing research into its agroforestry applications, biomass production potential, and carbon sequestration capabilities. The report notes that in Italy, studies on Paulownia invasiveness demonstrate that even in naturalization conditions, P. tomentosa is not able to permanently colonize the environment but does so only on a transitory basis.

THE HYBRID SOLUTION

At BioEconomy Solutions, we grow a fast-growing, high-yield, non-invasive, non-GMO hybrid Paulownia tree that represents the cutting edge of what this genus can offer.

Our hybrid is a trans-genera clone — not a genetically modified organism. As is the case with all trans-genera clones (think peach x apricot = sterile nectarine), it is seed-sterile and therefore non-invasive by design.

This is the same approach that Ray Allen, our mentor and the creator of the MegaFlora Paulownia hybrid, pioneered in the late 1990s. His work eventually led to the planting of over 17 million MegaFlora trees across 7 different provinces and 17 different locations in China — from the coast of Yantai all the way to the edge of the Gobi Desert, north to the border with Mongolia, and south to the border of Vietnam.

These trees were planted in desert environments. They were planted on degraded land. They were planted in conditions that most tree species could not survive. And they thrived.

The seed-sterile nature of our hybrid means that the primary concern raised about P. tomentosa — its prolific seed production and naturalization in disturbed areas — is simply not applicable. Our trees cannot spread beyond where they are intentionally planted. The invasive narrative does not apply.

THE GLOBAL FOOTPRINT

The video focuses exclusively on the eastern United States, where P. tomentosa has naturalized along roadsides and in disturbed areas. This is a legitimate regional concern for that specific species.

But the global picture is entirely different.

Paulownia trees are currently planted in over 60 countries across every major continent. The world regions and countries where Paulownia cultivation is documented include:

Asia: China (19 provinces), India, Japan, North Korea, Pakistan, South Korea, Taiwan, Turkey, Bhutan

Europe: Austria, Belgium, Croatia, Czechia, France, Germany, Hungary, Italy, Poland, Romania, Slovakia, Slovenia, Switzerland, United Kingdom, Southern Sweden, Denmark, Estonia, Lithuania, Ukraine, Scotland, Holland, Belgium, Luxemburg, Southern Greenland, Iceland

North America: 35 US states from Alabama to West Virginia

Oceania: Australia (5 states), New Zealand

South America: Argentina, Brazil, Guyana, Paraguay

Africa: Togo, South Africa, Kenya, Uganda, Morocco, Ghana, Namibia, Lesotho, Burkina Faso, Zimbabwe, Eswatini, Egypt

This is not the footprint of an invasive problem species. This is the footprint of a globally recognized, economically valuable, environmentally beneficial tree that governments, NGOs, corporations, and farmers around the world have chosen to cultivate intentionally.

The G.U.A.R.D.I.A.N. Framework™ E-BOOK – 58pages

THE ECONOMIC REALITY

Let us talk about what the video completely ignores: the extraordinary economic value of Paulownia cultivation.

In South Africa, one of our partners recently worked with a client who purchased just 1,000 trees for $5,000. The projected return on that investment? $200,000 — a 4,000% return on capital investment over approximately six years. In South African rand, that translates to approximately 3.6 million rand from just one and a half hectares of land.

In Mozambique, even with the cost of expensive irrigation infrastructure factored in, the cost per tree to grow and harvest came to approximately $18, with a return of $209 per tree after all costs. At 800 trees per hectare, that translates to potential returns of $145,000 to $200,000 per hectare including sawmill operations.

These are not theoretical projections. These are real numbers from real projects happening right now in real communities.

And the economic opportunity extends far beyond timber. BioEconomy Solutions has identified seven distinct revenue streams from a single Paulownia plantation:

- Carbon Credits — Paulownia sequesters 40-60 tons of CO2 per hectare annually, generating verified carbon credits that can be sold on voluntary and compliance markets

- Timber — Premium lightweight hardwood with the highest strength-to-weight ratio of any wood in the world

- Biochar — Converting biomass to biochar produces 2.57 to 3.26 carbon credits per ton, with biochar carbon credits trading at approximately $131-$165 per metric ton

- Biomass Energy — Green methanol, sustainable aviation fuel, biodiesel, bioethanol, and wood chips for heating

- Honey Production — Paulownia flowers for three months per year, with documented yields of up to one ton of honey per hectare

- Animal Fodder — Paulownia leaves contain 16% protein, 9% carbohydrates, and rich minerals, making them ideal for livestock feed

- Medicinal Compounds — Six major flavonoids identified in Paulownia flower extract, including apigenin, luteolin, and quercetin, with documented antioxidant, anti-inflammatory, and potential anticancer properties

Show us another tree that generates seven revenue streams simultaneously while also sequestering carbon, improving degraded soil, supporting biodiversity, and providing shade for companion crops.

You cannot. Because there is no other tree like it.

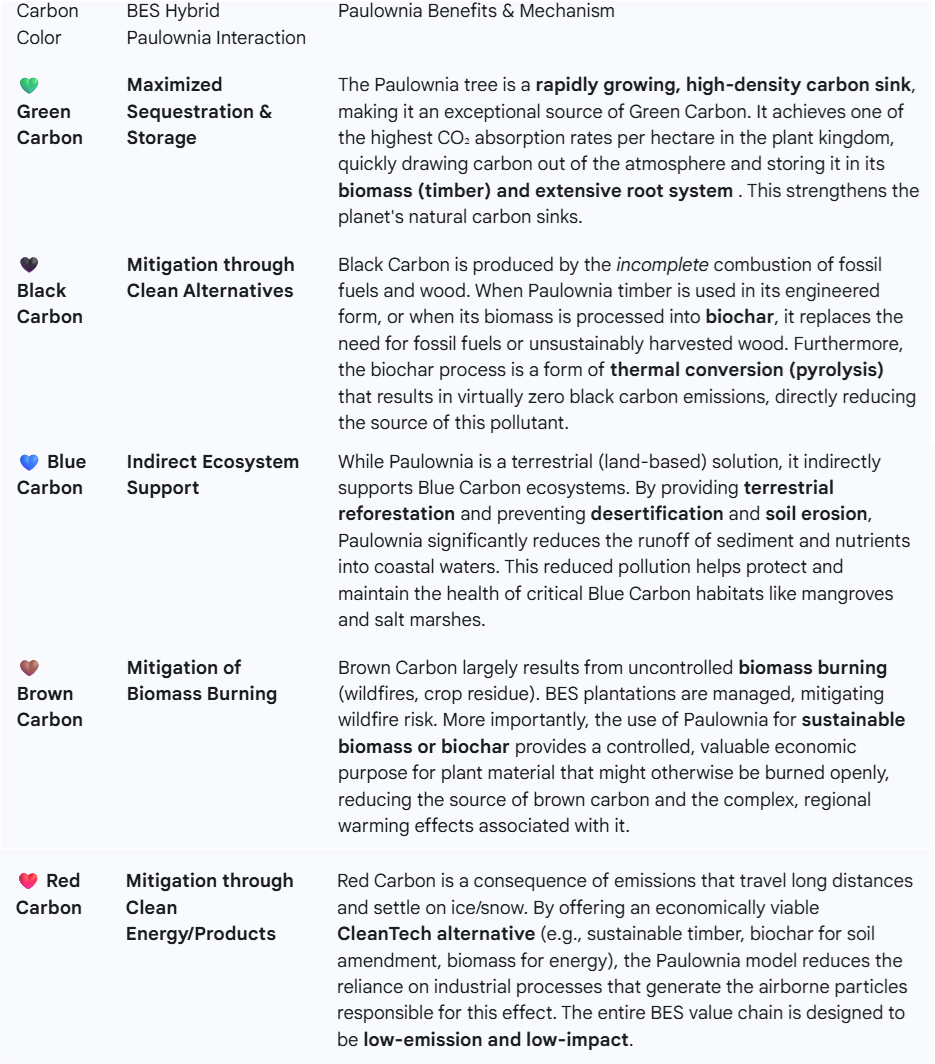

THE CARBON SEQUESTRATION CASE

The video mentions nothing about carbon sequestration. This is a significant omission given the current global climate context.

Paulownia is one of the most powerful carbon sequestration tools available to humanity right now. Here is why:

The Coppicing Advantage

Traditional carbon sequestration calculations assume you plant a tree once and harvest it once. But Paulownia is a coppicing tree — it regrows from its own stump after harvest, using the same well-established root system. This means:

- Plant once, harvest seven times

- Regrows from stumps in 90 days

- 5-year harvest cycles versus 50+ years for traditional trees

- Same root system supports multiple harvests

- 7x more carbon removal from the same land

The math changes everything. Instead of needing 1.48 trillion trees planted on a land area the size of the United States to address global carbon emissions, the coppicing model means you need far fewer trees achieving far greater impact over time.

The Biochar Permanence Factor

Living trees release CO2 when they burn or decay. But Paulownia biomass converted to biochar creates 1,000+ year carbon storage. This is the permanence factor that corporate carbon buyers — Microsoft, JPMorgan, Google — are increasingly demanding.

Biochar carbon credits saw demand double annually in 2023-2024, with prices averaging $150 per ton in 2024. By 2030, demand could be six times larger than supply. And 62% of high-quality biochar capacity for 2025 is already pre-sold via offtake agreements.

Paulownia, with its high cellulose content (50.55%), low ash content (8.9 g/kg), and gross heating value of 20.3 MJ/kg, is one of the most suitable feedstocks for biochar production available.

THE SOIL RESTORATION STORY

The video mentions that Paulownia can grow in disturbed soils as if this is a negative characteristic. In reality, it is one of the tree’s most valuable properties.

Paulownia’s deep taproot system — penetrating up to 40 feet into the ground — regulates the water table, removes soil salinity, and absorbs waste pollutants from agricultural facilities. Research has shown that P. elongata has potential for use as a swine waste utilization species, making it valuable in regions with high concentrations of swine and poultry industry.

The tree’s extensive root system helps improve soil structure, prevent erosion, and enhance water infiltration. Its large leaves, rich in nitrogen, fall and decompose to improve topsoil fertility. A 10-year-old tree produces 80 kg of dry leaves per year, providing natural green fertilizer.

In desertification projects around the world, Paulownia is being used to:

- Combat desertification in China’s Gobi Desert as part of the “Green Wall” project

- Restore degraded lands in Pakistan’s Punjab province

- Rehabilitate degraded lands in the Ethiopian Highlands

- Restore drylands in Spain’s Mediterranean region

- Support community-based land restoration in Kenya, Niger, and India

The Mully Foundation in Kenya planted 1.5 million trees and documented the creation of a microclimate — the reforestation literally changed local weather patterns, bringing rainfall back to areas that had experienced severe drought. Paulownia’s rapid growth rate means it can deliver these microclimate effects in 5-10 years rather than the 50+ years required by traditional species.

THE COMMUNITY DEVELOPMENT DIMENSION

The video frames Paulownia entirely as an ecological threat. It says nothing about what Paulownia cultivation means for communities.

In Mozambique, near the Chokwe area, three villages have been identified for a Paulownia-based community development project. These villages, where parents have left for the capital city to find work, leaving children with grandparents and no educational opportunities, will be transformed by the profits from Paulownia cultivation. Schools, clinics, sporting facilities, and skills development programs will be funded by the economic returns from the plantation.

In Botswana, the government has signed off on carbon trading agreements following COP29. The country’s largest diamond mine is funding a Paulownia carbon credit project, with the carbon credits going to the mine as offsets and the post-harvest timber revenue going to the local community. The community will own the entire plantation. The mine gets its carbon offsets for free. The community gets generational wealth.

This is what Paulownia can do when it is understood correctly. Not as an invasive weed to be eradicated, but as a tool for economic transformation, environmental restoration, and community development.

THE LUMBER TRUTH

The video does acknowledge Paulownia’s timber value, noting its use in furniture, musical instruments, surfboards, and guitar bodies. But it frames this as historical and speculative, suggesting the domestic market is small and the export market is uncertain.

The reality in 2025 is very different.

Paulownia lumber is increasingly recognized as the aluminum of lumber — lightweight yet strong, with the highest strength-to-weight ratio of any wood in the world. When comparing Paulownia with Balsa, it is approximately as light but twice as strong.

Its properties make it suitable for:

- Structural components — beams, poles, framing for non-load-bearing applications

- Interior finishing — paneling, trim, moldings, doors, window frames, cabinetry

- Flooring — dimensional stability and resistance to warping make it excellent for solid and engineered wood flooring

- Insulation — low density and excellent thermal insulation properties

- Soundproofing — acoustic panels for sound diffusion and absorption

- Outdoor structures — decks, fences, pergolas, saunas, pool decks

- Mass timber — CLT (Cross-Laminated Timber), Glulam, and engineered panels

The sandwich approach — a Paulownia core with a birch exterior — further increases structural strength while saving weight, opening up applications in mass timber construction that were previously unavailable to lightweight species.

China currently exports Paulownia window blinds around the world. The global demand for lightweight, sustainable, fast-growing hardwood is only increasing as traditional hardwood supplies from tropical forests continue to decline due to deforestation.

THE FIRE RESISTANCE FACTOR

One property the video completely ignores is Paulownia’s remarkable fire resistance.

Paulownia wood has an ignition temperature of 420-430°C, compared to the average hardwood ignition temperature of 220-225°C. This means Paulownia is nearly twice as resistant to ignition as conventional hardwoods.

Paulownia wood generates very little combustible gas when heated. It contains less lignin than cedar wood. These properties have made it the traditional material for clothing wardrobes in Japan for decades — the wood simply does not catch fire easily.

In an era of increasing wildfire risk driven by climate change, fire-resistant building materials are not a luxury. They are a necessity. Paulownia’s natural fire resistance makes it an increasingly valuable material for construction in fire-prone regions.

THE MEDICINAL DIMENSION

The video briefly mentions that Paulownia has been used in traditional Chinese medicine and that research has identified bioactive phytochemicals with potential anti-cancer properties. This is accurate, but the depth of the research goes far beyond what the video suggests.

Six major flavonoids have been identified in Paulownia flower extract:

- Apigenin — antioxidant, anti-inflammatory, and anticancer properties

- Diplacone — potential vasodilator, protects against vascular endothelial injury

- Mimulone — antioxidant and anti-inflammatory properties

- 5,4′-dihydroxy-7,3′-dimethoxyflavanone (DDF) — protection against oxidative stress

- Luteolin — antioxidant, anti-inflammatory, and anticancer properties

- Quercetin — antioxidant, anti-inflammatory, and antiviral properties

Paulownia flowers are also a rich source of polysaccharides with immunomodulatory and antioxidant activities. Recent research has explored ultrasound-assisted enzymatic extraction methods that show promising results for yield and quality.

The pharmaceutical and nutraceutical potential of Paulownia flowers represents an emerging revenue stream that is only beginning to be explored commercially. For centuries, Paulownia flowers have been used in Chinese medicine to treat bronchitis, enteritis, tonsillitis, and dysentery. The modern research is now validating what traditional practitioners have known for generations.

PART C — THE SHIFT: What This Means for You

Here is the lesson that this entire discussion teaches us.

The internet is not a reliable source for species-level botanical information.

When you search “Paulownia” online, you get P. tomentosa. You get invasive species warnings. You get removal guides. You get the same narrative repeated across hundreds of websites, all citing each other, all focused on the one species that has caused problems in one region of the world.

What you do not get — unless you know where to look — is the full picture. The 17 species. The non-invasive hybrids. The CABI guidance for UN carbon projects. The FAO commission reports. The peer-reviewed research from Fort Valley State University. The real-world plantation results from South Africa, Mozambique, Kenya, China, and 60 other countries.

This information gap has real consequences. It shapes policy. It influences investment decisions. It affects what landowners choose to plant. It determines which communities get access to economic transformation tools and which do not.

The future belongs to those who do their homework.

If you are a landowner considering Paulownia cultivation, do not let a YouTube video about P. tomentosa in the eastern United States make your decision for you. Research the specific species and hybrids available. Understand the soil requirements. Learn about the seven revenue streams. Talk to people who are actually growing and harvesting these trees commercially.

If you are an investor evaluating nature-based carbon solutions, understand that the Paulownia genus — specifically non-invasive hybrid and elongata species — represents one of the most compelling investment opportunities in the carbon removal space. The combination of rapid growth, coppicing capability, biochar production potential, and multiple revenue streams creates a risk-adjusted return profile that is difficult to match with any other biological asset.

If you are a corporate sustainability officer looking for verified, high-quality carbon credits that can withstand regulatory scrutiny and investor due diligence, Paulownia-based carbon projects offer the transparency, measurability, and permanence that the market increasingly demands.

And if you are simply someone who watched that YouTube video and came away thinking that Paulownia is nothing but an invasive weed — we hope this article has given you a more complete picture.

THE BOTTOM LINE

The video reviewed in this article is not wrong about P. tomentosa in North America. It is incomplete about Paulownia as a genus, as a global resource, and as one of the most powerful tools available for addressing the intersecting crises of climate change, land degradation, rural poverty, and sustainable development.

One species does not define a genus.

One region does not define a global resource.

One narrative does not define the truth.

Paulownia tomentosa is the black sheep of the Paulownia family. Every family has one. But you do not judge an entire family by its most difficult member. You do your homework. You look at the full picture. You ask the right questions.

At BioEconomy Solutions, we have been asking those questions since 2018. We grow non-invasive, non-GMO hybrid Paulownia trees on our farm in South Carolina. We process the lumber. We develop the markets. We build the carbon credit infrastructure. We work with partners across Africa, Asia, South America, and beyond to bring the full economic and environmental potential of this extraordinary tree to communities that need it most.

We are not just planting trees. We are building a bioeconomy. Brick by brick.

BEGIN THE CONVERSATION

What is the biggest misconception you have encountered about Paulownia trees in your region or industry?

Have you seen the invasive narrative affect investment decisions, land use policy, or community development projects in your area? We want to hear from you.

Drop a comment below, or reach out directly to begin a conversation about how Paulownia can work for your land, your investment portfolio, or your sustainability goals.

Only one of 17 kinds of paulowia species has issues. The one we grow is totally safe. Watch the video — it explains everything. Are you looking at paulownia for a project?

Visit us: bioeconomysolutions.com

📅 Book a consultation 📞call: www.BioEconomySolutions.com/bookcall

Email: mail@bioeconomysolutions.com

Phone: 843.305.4777

Get your free Paulownia Carbon Report — link in our featured section.

Repost this if you believe the full story of Paulownia deserves to be told.

Share this with a landowner, investor, or sustainability leader who needs to see the complete picture.

Tag someone who has been misled by the invasive narrative.

#Paulownia #Bioeconomy #CarbonCredits #SustainableForestry #NatureBasedSolutions #ESG #CircularEconomy #Agroforestry #CarbonSequestration #MassTimber #RegenerativeAgriculture #ClimateAction #ForestRestoration #BioEconomySolutions